Dear Sir,

This is with reference to the ‘Hips Don’t Lie’ lecture. There are a few doubts I have about this…

Firstly, this is what I understand about the two approaches (please correct me where I’m wrong):

An investment is ‘good’ if the present value of future cash-flows is greater than the price paid for it (the basic economic concept). Since future cash-flows have to be estimated, there is a risk that we may overestimate these cash-flows. To deal with this risk, we keep a margin of safety in the price that we are willing to pay for an investment. These points are common for both ‘value’ and ‘growth’ approaches.

Now, on the one hand, in the value approach, we keep a margin of safety by mainly relying on the current economic value of the firm’s assets and not so much on its future growth. We mainly try to value the existing assets of the firm and see if we can get an ‘interest’ in them at a cheap price. Graham’s 10 rules of return and risk largely point in this direction.

On the other hand, in the growth approach, we keep a margin of safety by mainly relying on the future growth prospects of the firm and not so much on current economic value of its assets. We try to estimate the future cash-flows of the firm based on our strong expectations of growth and see if we can get an ‘interest’ in these cash-flows at a cheap price.

The ‘value’ approach relies on cash-flow value of assets while the ‘growth’ approach relies on the cash-flow value of growth. Therefore, in using Graham’s approach, the nature or quality of a company’s business is not of critical importance but the quality of its assets is. On the other hand, using Fisher’s approach, the nature and quality of the business (including the management) is of prime importance and not the quality of its assets.

Now my question: when you say that the two approaches are ‘joined at the hip’, do you mean that they CAN be integrated into a better investment philosophy or they SHOULD be integrated to have any sort of philosophy at all?

To my mind, the two approaches are separate and can be effectively used separately. Even if someone is able to integrate them, at some point of time, there would have to be tradeoffs between the two approaches. When I say this, I’m thinking similar to Michael Porter’s model of basic strategic orientation of firms: Low Cost OR Differentiation. A firm cannot be both: a low-cost operator as well as a differentiator, at the same time. It has to make a trade-off and focus on one approach as a provider of ‘sustainable competitive advantage’ this is because the two approaches are mutually exclusive. This does not mean that a low cost operator should completely ignore differentiation and vice-versa. What it only means that in the end, a firm can focus on only one approach from which to derive its competitive advantage.

Similarly, can an investor, psychologically and intellectually, handle the diverse demands of the ‘growth’ approach and the ‘value’ approach? Will he not have to eventually make trade-offs, in his investment philosophy, towards one approach, at the expense of the other? The expertise required to pick a good value stock and a good growth stock are probably very different. Should one try to achieve both? It is certainly desirable to be able to do both.

But is it feasible?

Sincerely yours,

K.K

_____________________________________________________________________________________

Dear K.K,

I think it is feasible to have your cake and eat it too :-)

You made some excellent points.

Graham's approach - often called the value approach was based on “protection” instead of “prediction”. He was never a believer in forecasting financial statements beyond a year or two. Rather, he focused on getting something that was cheap today based either on asset valuation, or on earning power valuation, WITHOUT making optimistic growth projections about that future earning power.

The key thing to remember is that Graham never really valued a business or a stock. Rather he insisted on a large margin of safety i.e. proof that the price was he was paying was much less than the value that he was receiving, whatever that value may be. Moreover, his extreme diversification took care of mistakes of commission.

In the modern context, many Grahamites, including me, have evolved Graham's approach to incorporate growth expectations in our investment process. Basically, we are so spoilt by Graham that we like getting free lunches and having our cakes and eating them too :-)

Seriously, we DON'T pay for growth. We are aware that some businesses have a great growth potential but we don't want to PAY for that growth. So we like to buy growth stocks at prices which imply low or negative earnings growth.

Read the following very interesting document which will hopefully resolve your questions. If not, please revert.

http://tinyurl.com/y9h252

SB

___________________________________________________________________________________

Dear Sir,

The speech you sent does indeed explain the ‘have your cake and eat it too’ approach. In essence what you and Mr. Nygren are saying is: take Graham’s value approach and apply another ‘filter’ of growth to these value stocks. The ones which emerge out of this double selection criterion are good stocks for investment.

So the approach is essentially value investing with an additional safety buffer called growth. You are not looking for high-growth stocks and buying them almost regardless of the price because the high internal rate of return will make up for a steep valuation today, given sufficient time.

So, I’m probably beginning to understand the idea behind value and growth approaches being ‘joined at the hip’.

K.K

Thursday, December 21, 2006

Thursday, November 09, 2006

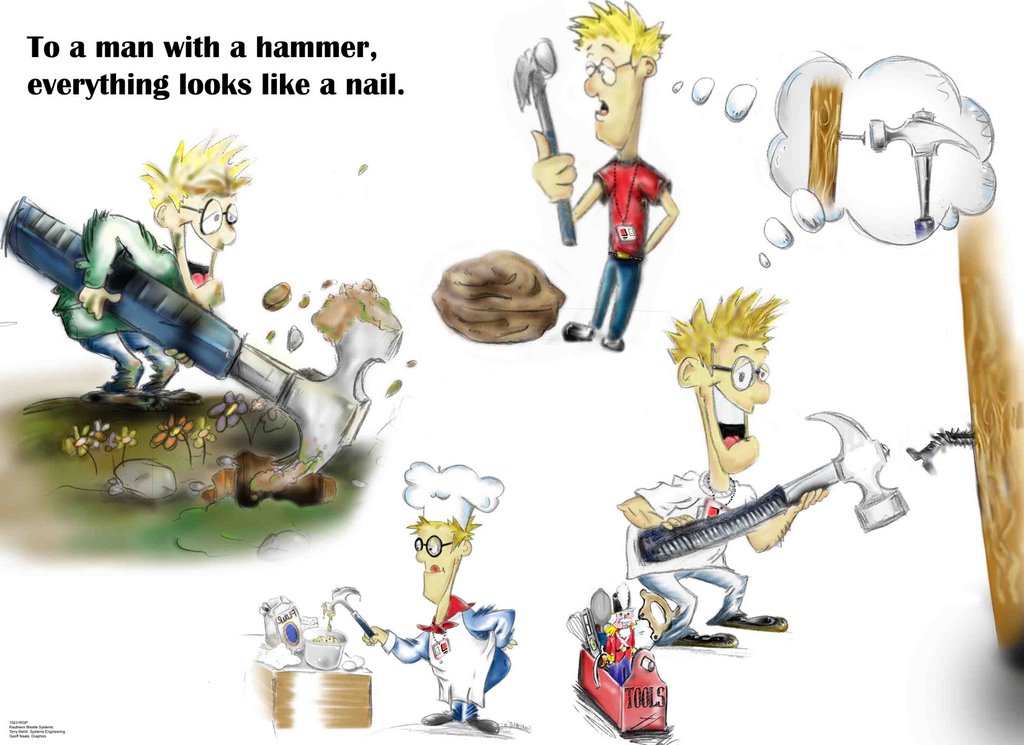

Are CFO's Men with Hammers?

The following is the text of an article I wrote recently for a publication meant for CFOs. The article was withdrawn before publication.

Are CFO's Men with Hammers?

{kind=link}

I often ask my students the following question:

You are the CFO of a textile company which makes commodity yarn. The industry in which you operate is extremely competitive beset with excess capacity.

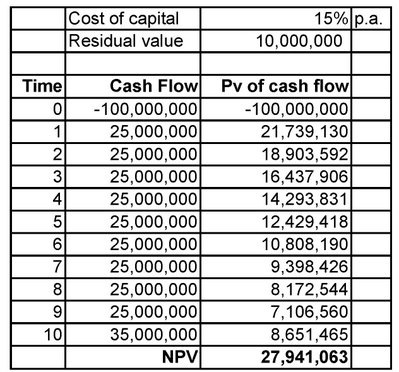

A leading textile machinery manufacturer’s marketing agent approaches you with a proposal to sell you a new loom which is more efficient than any other loom available in the market. He informs you that the new invention is far more efficient and that it will save your company a substantial sum of money every year, so that it will pay for itself in a very short span of time. To justify his claims, he presents you with the following figures: (1) Cost of machine: $100 million.; (2) expected life = 10 years; (3) annual savings in operating costs for the next 10 years = $25 million. p.a.; (4) expected residual value of the machine = $10 million.

You have verified the numbers presented to you and find them to be accurate. Your company’s pre-tax hurdle rate is 15% p.a.

Should your company place orders to buy these looms?

Using their newly-acquired skills in DCF analysis, the students quickly determine the NPV, which is large and positive, and conclude that the loom should be purchased and installed as soon as possible.

The main problem with this approach is that it often leads to wrong conclusions arising out of over-use of the DCF model in finance and ignorance of appropriate models from other disciplines such as microeconomics, game theory, and psychology.

Warren Buffett, the world’s most respected investor and Chairman of Berkshire Hathaway Inc., and his partner, Charlie Munger, call this “the man with a hammer syndrome”: To a man with a hammer everything looks like a nail. If all you have is one tool, you’re going to end up overusing it.

How can one deal with the man with a hammer syndrome? Well, the best way, according to Mr. Munger, is to train oneself to “jump jurisdictional boundaries” and grab the most appropriate models from multiple disciplines that best solve the problem at hand.

The present problem requires a two-step analysis drawing on models from multiple disciplines before drawing any conclusions.

The first step involves using DCF analysis, which my students have no problem with. That part of the analysis has already been done and described above.

It’s the second part of the analysis which they miss. They miss it because they are not yet trained to think in a multi-disciplinary manner.

That second part of the analysis requires them to answer the following question: How much of the cost savings that the new loom will deliver be kept by the company and how much of it will be passed on to the company’s customers?

Ah ha! Now it gets a bit tricky, doesn’t it? It gets tricky because to answer that question one has to grab models from microeconomics – such as the model of competition. And, of course, when you look at it from that angle, its obvious, that given the nature of textile industry’s competitive nature, arising out of surplus capacity and commodity attributes of the product, most of the cost-savings from the new loom will go to the customers of the company, and not to its owners.

This will happen because once a textile company acquires the new loom and achieves the promised cost savings, it will tend to either lower its prices to gain market share, or keep prices unchanged to earn higher margins.

Sooner or later either of these two actions would get noticed by the company’s competitors and they would naturally rush to make the same investments in new, efficient looms, in order to regain lost market share or to earn higher margins. Ironically, the very salesman who sold the loom to your textile company will rush to sell it to your second competitor and then the third one and so on, citing your own cost saving experience as reason for your competitors to buy his company’s new invention. After all, he is not in the business to make your production process more efficient. He is in the business of making money for his company (“Whose bread I eat, his song I sing”).

In our problem, competition i.e. the absence of a cartel will ensure that almost all of the efficiency gains end up in the pockets of the buyers of textiles, and not in the pockets of the owners of the textile companies.

Another irony arises out of the fact that this tragic outcome would occur even though all of the promised efficiency gains materialized. It’s not that the new looms aren’t any good. In fact they are so good that any advantage for the early buyers will prove to be a temporary illusion because sooner or later everyone has to have one or risk being perished.

Such is the nature of certain businesses where you have to keep on putting more and more money in just to stay where you are. (It's like running up on an escalator which is moving down - lots of investment, zero progress). You keep on investing money in projects which have positive NPVs and high IRRs and still end up earning substandard returns on capital that destroy shareholder value.

On the other hand, if we were dealing with India's largest tobacco company like ITC, a virtual monopoly where the buyers of its cigarettes are price-insensitive addicts – if someone sold it a more efficient machine to make its cigarettes - then the cost savings from this new wonderful invention will not be passed on to the customers. Rather, much of the post-tax cost savings would accrue to the benefit of ITC’s shareholders.

So, without jumping over the jurisdictional boundary of finance where DCF resides, into the jurisdictional boundary of microeconomics where the model of competition resides, you cannot solve the problem at hand in a satisfactory manner.

In early 1980s, Mr. Buffett faced a similar dilemma in the management of the unprofitable textile business of Berkshire Hathaway. He knew that the US textile industry was going to become increasingly uncompetitive, primarily due to its high, and impossible to reduce, labor costs. He also knew that he had other opportunities in which he could invest capital where the prospects of earning superior returns were excellent, given the fundamental economics of those businesses then available.

Long before most capitalists would even consider the possibility, in 1985, Mr. Buffett decided to shut down the textile operations of Berkshire and redeploy the capital in great businesses. It proved to be one of the best business decisions he ever made. In a letter written to the shareholders of Berkshire in 1985, Mr. Buffett reasoned:

“The promised benefits from these textile investments were illusory. Many of our competitors, both domestic and foreign, were stepping up to the same kind of expenditures and, once enough companies did so, their reduced costs became the baseline for reduced prices industry wide. Viewed individually, each company’s capital investment decision appeared cost effective and rational; viewed collectively; the decisions neutralized each other and were irrational (just as happens when each person watching a parade decides he can see a little better if he stands on tiptoes). After each round of investment, all the players had more money in the game and returns remained anemic.”

Mr. Buffett utilized the metaphor of a parade to illustrate a well-known problem in game theory called “Prisoner’s Dilemma.”

Prisoner’s dilemma involves two suspects, A and B, who have been arrested by the police. The police have insufficient evidence for a conviction, and, after separated both prisoners, offer each the same deal: if one testifies for the prosecution against the other and the other remains silent, the betrayer goes free and the silent accomplice receives the full 10-year sentence. If both stay silent, the police can sentence both prisoners to only six months in jail for a minor charge. If each betrays the other, each will receive a two-year sentence. Each prisoner must make the choice of whether to betray the other or to remain silent. However, neither prisoner knows for sure what choice the other prisoner will make. So the question this dilemma poses is: What will happen? How will the prisoners act? The dilemma is summarized in the following table:

The dilemma arises when one assumes that both prisoners only care about minimizing their own jail terms. Each prisoner has two options: to cooperate with his accomplice and stay quiet, or to defect from their implied pact and betray his accomplice in return for a lighter sentence. The outcome of each choice depends on the choice of the accomplice, but the player must choose without knowing what their accomplice has chosen to do.

Let's assume prisoner A is working out his best move. If his partner stays quiet, his best move is to betray as he then walks free instead of receiving the minor sentence. If his partner betrays, his best move is still to betray, as by doing it he receives a relatively lesser sentence than staying silent. At the same time, the other prisoner's thinking would also have arrived at the same conclusion and would therefore also betray.

If reasoned from the perspective of the optimal outcome for the group (of two prisoners), the correct choice would be for both prisoners to cooperate with each other, as this would reduce the total jail time served by the group to one year total. Any other decision would be worse for the two prisoners considered together. When the prisoners both betray each other, each prisoner achieves a worse outcome than if they had cooperated.

In other words, actions that appear to be rational from an individual’s perspective sometimes become foolish, when viewed from a group’s perspective. The functional equivalent of the prisoner’s dilemma in our problem creates miserable choices but would we have discovered that unless we had jumped over into the jurisdictional boundary of game theory? I think not.

So, we grabbed DCF from finance, and then jumped over its jurisdictional boundary into the territory called microeconomics, where we grabbed competition. Then we jumped over the fence again and grabbed prisoner’s dilemma from game theory.

We need one more jump into the jurisdiction of psychology. And then we can stop jumping around and solve the problem.

One model we will grab from psychology is what Mr. Munger calls “bias from commitment and consistency.” When you have already made prior commitments to pet projects, you may find it hard, even impossible, to reverse your position and change course. If old reasons are no longer valid to support the original decision, new ones shall be invented. Man, after all, is not a rational animal, but a rationalizing one.

Another model we will grab from psychology is called the “contrast effect”. One version of the contrast effect makes small, incremental escalations in commitments go un-noticed, particularly when these escalations are carried out over a long period of time.

It works in Chinese brainwashing techniques. It also contributes to foolish business decisions.

If you’ve already sunk in $1oo million in a bad capital investment project, an additional investment of $10 million will look very small in contrast to the much bigger total commitment already made and will therefore tend to go un-noticed.

This version of contrast effect is also called the "boiling frog syndrome": If you put a frog in boiling hot water, it will jump out instantly, but if you put a frog in room-temperature water and then slowly heat it, it will boil and die.

The story about the boiling frog isn’t true. That metaphor, however, is highly appropriate because the human equivalent of the boiling frog is there in all of us.

Mr. Buffett could see that bias from commitment and consistency and the boiling frog syndrome from psychology often combine with the prisoners’ dilemma model from game theory, making many a businessman take foolish decisions by continuing to sink more and more money in a lousy business instead of taking money out and re-deploying it more productively elsewhere. He realized that in some industries the chief problem is that if you continue to remain in the game then “you can’t be a lot smarter than your dumbest competitor”.

And, so, Mr. Buffett wisely refused to play this game and withdrew his capital from the textile business and re-invested the proceeds in businesses with much better fundamental economics like Coke, Gillette, Capital Cities, See’s Candies, and Nebraska Furniture Mart. Over time, his decisions to shut down the textile operations of Berkshire and to re-allocate the released capital elsewhere have made its shareholders richer by tens of billions of dollars.

Mr. Buffett’s multi-disciplinary mind helped him solve a complex business problem. I see no reason why CFOs cannot apply the same thinking style in solving complex business problems they face.

Otherwise, they are destined to remain as “men with hammers”.

Thursday, October 26, 2006

Project Libra Revealed

In 2001, I and one of my great friends Nalin, were working on a secret project. We decided to call it "Project Libra". The Project involved exploring ideas for unlocking value from a company which I thought was highly undervalued.

While preparing for a lecture today, I came across the transcript of a chat I had with Nalin on Project Libra. This chat took place on 19 May, 2001. I reproduce here the transcript of that chat. I decided not to edit anything out or make any corrections whatsoever.

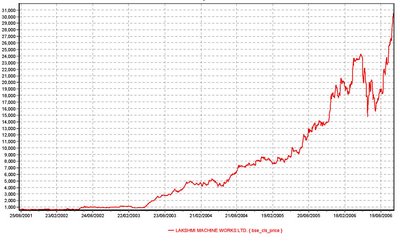

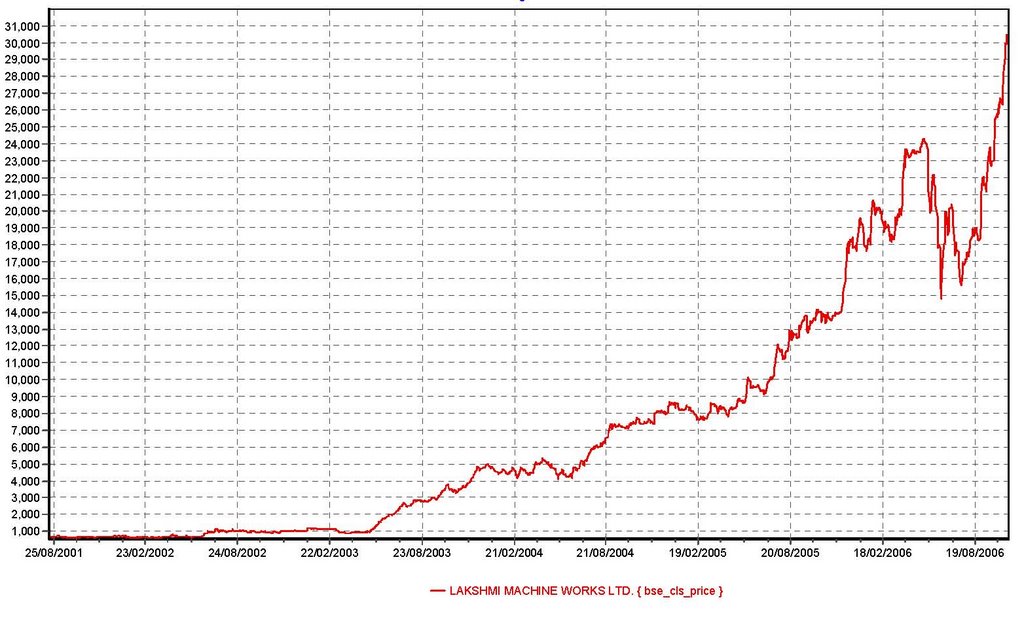

At the end of the transcript, I have placed a stock price chart of the company from around the time of that chat till recently. It became a 35-bagger. The company's name is Lakshmi Machine Works.

Chat

Date: May 19 2001 - 11:58am

Sanjay says:

Hi Nalin, will try to send Libra comments thru MSN

Nalin says:

Okay - send

Waiting for Nalin to accept the file "Libra Comments.htm" (4 Kb, less than 1 minute with a 28.8 modem). Please wait for a response or Cancel (Alt+Q) the file transfer.

Transfer of file "Libra Comments.htm" has been accepted by Nalin. Starting transfer...

Transfer of "Libra Comments.htm" is complete.

Nalin says:

Okay got it. Tell me when you send the Libra stuff. Bye

Sanjay says:

Wait

Nalin says:

waiting

Sanjay says:

is the file legible. it may not be i am sending a text version

Nalin says:

okay send

Waiting for Nalin to accept the file "Libra comments.txt" (4 Kb, less than 1 minute with a 28.8 modem). Please wait for a response or Cancel (Alt+Q) the file transfer.

Transfer of file "Libra comments.txt" has been accepted by Nalin. Starting transfer...

Transfer of "Libra comments.txt" is complete.

Sanjay says:

will SMS u when ready with Taurus comments

Nalin says:

Got it thanx. Actually I don't remember myself if Rieter was under hostile takeover. Remember I told you in Delhi about a Swiss activist investor. Do you remember which company he was trying to acquire - why is Rieter or some other ?

Sanjay says:

That guy sold stake a pharma co to another pharma co

Nalin says:

Okay - anyway I had already deleted the hostile takeover reference.

Sanjay says:

OK spend a couple of minuts reading my note. I'm waiting

Nalin says:

Okay

Nalin says:

I'm still reading it - but I have one question - maybe you can answer while I continue reading - why should normal dep be 50% of dep charged ?

Nalin says:

Also, on the financial engineering thing - if you took out Rs 100 Crore from the company (by replacing it with debt) it won't earn 45 Cr of discretionary profit a year.

Nalin says:

I agree, in general, that financial engineering can add value. But only when cash earnings. (They may already be stable - but we're not sure of that yet). Also, financial engineering in India is a very difficult task - and an acquirer would not want to pay now for benefits of financial engineering which he'll do post acquisition.

Sanjay says:

Take a look at the gross block and the accumulated depreciation. Gross block is 603 cr and acc dep is 407 cr. They are definitely overproviding depreciation. The amount of money that would be required to replace this gross block is definitely a lot more than the net block figure of 196 cr

Nalin says:

Sorry I missed a work in that message. I meant to say "But only when cash earnings are stable"

Nalin says:

If you feel that they are overproviding dep, then that is an additional upside which we will find out in detailed due diligence (if we are ever allowed to do that ) - at this stage its just a guess - we can't expect someone to pay top dollar for a guess.

Nalin says:

For all we know their assets might need a major revamp - which they have been delaying. Also in cash earnings we must deduct their increasing need for working capital

Sanjay says:

I am quite confident of the overprovision. Take a look at all the cash they have squandered away thru stupid diversification over all these years. THow did they finance it? not from new issue of shares, but from debt and internal accruals. Basically they had too much cash and insteadd of returning it to stockholders they simply threw it away

Nalin says:

You are right they might have overprovided depreciation. Do you want to base our presentation on that premise. Are you sure enough to make it a KEY assumption ?

Nalin says:

I'd rather just make it an additional upside

Sanjay says:

Not at all. What I want is to inform our investor group that this is classic case of massive misallocation of cash generated from operations. And that a rational person in control will have an opportunity to correct that misallocation and create value

Sanjay says:

Fine, you'can make it an additional upside but I should be in the document

Nalin says:

Okay - so we make that an upside that an acquirer gets - when he gains control. But I don't think we should ask him to pay for an upside - that we have no way of proving at this stage.

Nalin says:

Then the strategy remains more or less unchanged ?

Sanjay says:

Please also notice that my additional debt of Rs 100 cr requires an annual interest outgo of only Rs 15 cr and I have assumed c discretionary cash earnings of 45 cr p.a. at least until TUF benefits are available for the next three years. Even if the discretionary earnigns come to less than 45 cr, I can still pay a Rs 100 cr dividend financed out of from borrowed funds because the company is hugely

Sanjay says:

underleveraged.

Sanjay says:

Therefor I can bring my effecive cost of acqusition to Rs 18 cr for a 40% stake

Nalin says:

Like I said earlier - financial engineering is not something an acquirer will pay for up front

Sanjay says:

Why not? I would if I was certain of the benefits. If we get more info on the company's cash generating abilites then I would very gladly pay for financial engerring value

Nalin says:

In some cases it makes sense to go to the hilt in paying. In this case it makes sense to pay as little as possible - and not factor in too many upsides

Nalin says:

How do you get certain of the benefits ?

Sanjay says:

I agree with the conservatinve approach u are taking but putting a value equal to 100% of adjusted book value is too conservative, I feel.

Sanjay says:

We go to Coimbatore on a fact finding mission. we can control costs by travelling by train

Nalin says:

Its conservative - but in this case, paying more doesn't achieve much additional advantage - it disproportionately increases our downside risk. If we stick to market price in our bids - we have almost zero risk of loss - and a considerable upside.

Nalin says:

Even getting control of this company is very difficult - with labour, politics etc involved. Also, it probably has liabilities we haven't even dreamed off - such as corp guarantees for the steel project. Its a mess we don't want.

Sanjay says:

Ok think of it this way. Suppose, the amount of cash that can be taken out of this company without hurting it is only Rs 35 cr p.a. for the next three years and we are use a discolunt rate of 20% p.a. Then the present value of the next three year cash flows alone comes to Rs 650 per share.

Nalin says:

Its pure GM - with controlled downside risks

Sanjay says:

Nalin how can we do a successful GM when we are delaing with promoters who are not cash rich? I thought u did that cash rich promoters

Nalin says:

Listen - the way the industry is going - the company may need to get cash negative - to be able to emerge a strong player

Sanjay says:

But we'll be out well before that happens

Nalin says:

How do you get out ?

Sanjay says:

Leveraged recap can esnure that our cost is negligible. Then whatever we sell the company for is profit

Nalin says:

You can't do a leveraged re-cap if we fear uncertain cash flows - because of a recession + competition. Depending only on the TDF is not enough.

Sanjay says:

To quote u, "I agree to disagree!"

Nalin says:

But what strategy do we put in the book

Sanjay says:

I guess it would be best if we were to fix the meeting for wednesday and I come to mumbai on Monday and we spend 2 days on it

Sanjay says:

Im ust tell u that I am enjoying working with u

Nalin says:

Thats good.

Nalin says:

Lets give one last attempt at coming to consensus now.

Nalin says:

Tell me why is my strategy flawed. Let me defend it for a change.

Sanjay says:

It all comes down to valuation. You are being unlta conservative in valuing this company. A company that produces a cash profit of 70 cr cannot be worth less than the book value of 117 cr. This is true even if a large part of those earnings are not discretionary.

Nalin says:

I'm not saying its not worth more - I'm just saying we shouldn't pay more - what's wrong with sticking to a low price ?

Sanjay says:

Your views on valuation in the presentation are so pessimistic that the whole project will turn off investors

Sanjay says:

and I thought u were an investment banker!

Nalin says:

I WAS an investment banker. Now I think more like a value investor.

Nalin says:

My views on valuation were given on the next page - where I said that it could be worth Rs 1800

Nalin says:

Did you get the presentation ?

Sanjay says:

LOL! i agree we sohuld pay less if we can get away with it but how to achieve it is the issue here. We cannot do this deal unless we convince investors that this is a sitting duck

Nalin says:

But did you get the presentation - I hope you aren't refering only to my initial note

Sanjay says:

That 1800 is based on relative valuation with peers, something that may be difficut to sell to our investors.

Nalin says:

Before I proceed I need to know if you got the presentation

Sanjay says:

I got the presentation. Also, our strategy shoudl reflect the illiquidity of the stock for exit. We cannot sell a deal to investor on the basis that one of the exit routes will be thru the market when dailty volume is 15 shares. We cannot also tell them to hold it as a value stock. Our investors want to make a quick buck.

Nalin says:

I mentioned exit through the market only when the deal is on (and only to a very limited extent). I mentioned illiquidity when I said only 32,000 shares were traded last year.

Nalin says:

Holding on to the stock is a worst case scenario. I think we shouldn't proceed unless we have an investor who is willing to take that risk. Because its a real risk. I can think of no other approach which has a lower risk.

Sanjay says:

The stock is so illiquid that mkt operations after Public Annoucement will not be feasible. under such circumstances, why not have a conditional two-tiered tender offer which guarantees either control or exit thru tender in their counter offer?

Nalin says:

Let me think about this for a minute ?

Sanjay says:

Say a 7% toehold at 850, a 21% offer at 1500 subject to minumum level of acceptance of 20% with a lower offer price of 850 if shares tendered are less than 21%

Nalin says:

I think the problem again will be return on investment. We did this exercise in Taurus. The return on investment was just too low

Nalin says:

What should be the offer size ?

Sanjay says:

The toehold will cost only Rs 7 cr. A 21% offer will cost 38 cr., 50% of which or 19 cr will be cash escrow

Nalin says:

You are saying a 21% conditional offer, with 20% minimum acceptance ?

Sanjay says:

yes

Nalin says:

But in terms of risk - how is this different from what I said. You still run the risk of getting stuck with acceptances in your offer at Rs 850 ? But the downside is that return on investment goes for a toss. It was bad enough under my option at only 50% annualised.

Nalin says:

You also run the risk of actually getting 21% at Rs 1500

Nalin says:

Are you saying the only problem with my plan is that we won't get an investor willing to take the risk of a residuary holding at Rs 850 ?

Sanjay says:

I am unable to explain. Either we have to meet or I have prepare a note on bidding strategy explaining why I think that a conditional offer may make sense. The main reason is that a conditional offer is a hedge. But it imposes an ban on market purchases. But mkt purchases are not going to happen in any case in this stock/

Nalin says:

Okay - we'll discuss conditional offers later. Lets go back to why my plan is flawed ?

Sanjay says:

Look at pg 18. What if they don't buy us out? What if they go to instutions and get them to not tender to us because of lack of significant premium to market offer fro us. There are 100 shares. 13+21+33 (rieter,promoter,instutions) or 67 will not come. 20 shares are are missing. therefore 87 will not come. we already have say 7%. so we'll get only 6% if institutions do not tender.

Sanjay says:

they can simply ignore us and just get institutions to not tender.

Sanjay says:

so we end up with 13% at 850 and no control just apin in their necks

Sanjay says:

in order to get the institutions to tender we have to offer a significant premium to market otherwise they will have an excuse for not tendering. I saw this in Gesco case

Sanjay says:

If institutions do not tender and they don't make a counter offer we are fucked

Nalin says:

There is only a small chance that FIs will pre-agree not to tender. I think FIs will keep quiet about their intentions - therefore LIBRA will be forced to act. Also Rieter may want to ext. I don't think Libra will ignore us because they will not want to take any chances of losing control.

Nalin says:

But assuming this happens (its only a 2% chance) then our max downside is we are stuck with a 15% stake at 850. In other options there are worse risks.

Sanjay says:

In case of Gesco, the institutions made it very clear that they will not tender unless they got book value. In Gesco the book value was 54 and return on equity was less than 5%. So we told them that the stock is not worth book value because ROI is so poor. Thay told us to fuck off and come back with a 54 offer.

Sanjay says:

In LIBRA book value is 2000 even though a lot of it is water, but it does give a huge excuse to institutions to not tender. Also there is a history of this stock which at one tiem sold for Rs 10,000

Nalin says:

FIs will certainly want to put pressure on LIbra to give a better counter offer. They won't want to give them guaranteed comfort - and suggest they don't need to counter offer. Rieter will also want a higher counter offer - so there won't be any guarantees from that end eithre

Nalin says:

Anyway - we are talking about the same flaw - the chance (in my opinion small) of a residuary stake at Rs 850 ? Is there any other flaw ?

Sanjay says:

Precisely the point. In order to put this company in play we have to make institutions the sellers. Once we do that with our offer then our offer is the minimum they would get and they would demand higher from promoters or Rieter.

Sanjay says:

Unless we induce instutions to sell, we cannot succeed. becasue in any proxy contrest tyhey would side with management

Nalin says:

Okay - but we have to be careful not to introduce higher risks just to eliminate that risk - also be careful not to dilute returns too much. If you can come up with such a plan good. If we can't - we scrap this project.

Sanjay says:

My basic difference with you on this is that u are approaching it as a GM operation, whereas I am appraoching it as an acqusition prior to a leveraged recap, but which could also become a GM operation.

Sanjay says:

Hopefully it will be the later

Nalin says:

I strongly feel that we should not acquire this company - but stick to GM

Sanjay says:

But even if it turns out to be the former, I can do a recap to get my cost to negligible levels

Nalin says:

Do you want to discuss GM vs acquisition a little more ?

Sanjay says:

OK

Sanjay says:

Let's talk about promoters. GM is done with cash rich guys not poor ones

Sanjay says:

thesze guys are leveraging to creep up. OK, chola may be a white knight in which case our probability of GM is that much higher

Nalin says:

Overgeneralisations are dangerous. Every situation is different. In this case, we keep the cash required to buy us out low - so that they can actually buy us out - therefore a low bid

Sanjay says:

u do have a point there

Nalin says:

If Cholamandalam is appears as a white knight and gives a counter offer without buying us out - we lose - but hopefully without a loss.

Nalin says:

Also please note if we start a bidding match, Cholamandalam can still come in - in that case our losses would be even higher

Sanjay says:

now u're making sense

Sanjay says:

what 2 do?

Sanjay says:

OK, here;s a plan, we go with your presentation with John and ASit and see how they feel about it. Do u want to talk to Asit about Libra?

Sanjay says:

On pg 19 of your presentation u mention, "If promoters do not give counter offer - we become largest shareholder". I don't agree with this because we will not have significant tenders at a low price offer if institutions are not participating

Nalin says:

Listen I don't want to steamroll you into this. So you keep thinking. I'll keep working on the presentation. Overall, I think we should give both plans to Asit and John, just to show that we have more ideas where Taurus came from. On whether the plan is good or not - we can decide tomorrow

Nalin says:

Okay - I'll take care of that

Sanjay says:

Just think about this aspct

Nalin says:

Yes - this requires a lot of thinking - I agree

Nalin says:

Earlier when I said we should give both plans to Asit _ I meant both projects not both plans

Nalin says:

Someone has just sent me an email from gescocorp. Should I check and see ?

Sanjay says:

WHATTT????

Nalin says:

Wait I'm checking

Nalin says:

A friend of mine has just joined Gesco Corp. He's coming to visit tomorrow. How wierd.

Sanjay says:

Don't tell him about me!

Nalin says:

I have this feeling that destiny is just a game played for God's perverse amusement

Nalin says:

I won't.

Sanjay says:

I wanna live

Nalin says:

Okay.

Sanjay says:

ask him what's happening in the company

Nalin says:

Any more detailed comments on Libra - such as page 19 ?

Nalin says:

I'll work on another draft of the presentation and send it to you - in the meantime you think strategy. But hurry up with Taurus. Because I need to print the presentation today

Sanjay says:

OK Give me 2 hours on Taurus. I agree with most of your work there, just a few points I want to add/amend

Nalin says:

Okay talk to you later then ?

Sanjay says:

In libra disagreement is on valuation, and accoringly on strategy, but i see your point that a alow priced offer will enable the promoters to buy us out at a lower cost

Sanjay says:

Bye?

Nalin says:

It was a stimulating discussion anyway. Bye.

Sanjay says:

bye

While preparing for a lecture today, I came across the transcript of a chat I had with Nalin on Project Libra. This chat took place on 19 May, 2001. I reproduce here the transcript of that chat. I decided not to edit anything out or make any corrections whatsoever.

At the end of the transcript, I have placed a stock price chart of the company from around the time of that chat till recently. It became a 35-bagger. The company's name is Lakshmi Machine Works.

Chat

Date: May 19 2001 - 11:58am

Sanjay says:

Hi Nalin, will try to send Libra comments thru MSN

Nalin says:

Okay - send

Waiting for Nalin to accept the file "Libra Comments.htm" (4 Kb, less than 1 minute with a 28.8 modem). Please wait for a response or Cancel (Alt+Q) the file transfer.

Transfer of file "Libra Comments.htm" has been accepted by Nalin. Starting transfer...

Transfer of "Libra Comments.htm" is complete.

Nalin says:

Okay got it. Tell me when you send the Libra stuff. Bye

Sanjay says:

Wait

Nalin says:

waiting

Sanjay says:

is the file legible. it may not be i am sending a text version

Nalin says:

okay send

Waiting for Nalin to accept the file "Libra comments.txt" (4 Kb, less than 1 minute with a 28.8 modem). Please wait for a response or Cancel (Alt+Q) the file transfer.

Transfer of file "Libra comments.txt" has been accepted by Nalin. Starting transfer...

Transfer of "Libra comments.txt" is complete.

Sanjay says:

will SMS u when ready with Taurus comments

Nalin says:

Got it thanx. Actually I don't remember myself if Rieter was under hostile takeover. Remember I told you in Delhi about a Swiss activist investor. Do you remember which company he was trying to acquire - why is Rieter or some other ?

Sanjay says:

That guy sold stake a pharma co to another pharma co

Nalin says:

Okay - anyway I had already deleted the hostile takeover reference.

Sanjay says:

OK spend a couple of minuts reading my note. I'm waiting

Nalin says:

Okay

Nalin says:

I'm still reading it - but I have one question - maybe you can answer while I continue reading - why should normal dep be 50% of dep charged ?

Nalin says:

Also, on the financial engineering thing - if you took out Rs 100 Crore from the company (by replacing it with debt) it won't earn 45 Cr of discretionary profit a year.

Nalin says:

I agree, in general, that financial engineering can add value. But only when cash earnings. (They may already be stable - but we're not sure of that yet). Also, financial engineering in India is a very difficult task - and an acquirer would not want to pay now for benefits of financial engineering which he'll do post acquisition.

Sanjay says:

Take a look at the gross block and the accumulated depreciation. Gross block is 603 cr and acc dep is 407 cr. They are definitely overproviding depreciation. The amount of money that would be required to replace this gross block is definitely a lot more than the net block figure of 196 cr

Nalin says:

Sorry I missed a work in that message. I meant to say "But only when cash earnings are stable"

Nalin says:

If you feel that they are overproviding dep, then that is an additional upside which we will find out in detailed due diligence (if we are ever allowed to do that ) - at this stage its just a guess - we can't expect someone to pay top dollar for a guess.

Nalin says:

For all we know their assets might need a major revamp - which they have been delaying. Also in cash earnings we must deduct their increasing need for working capital

Sanjay says:

I am quite confident of the overprovision. Take a look at all the cash they have squandered away thru stupid diversification over all these years. THow did they finance it? not from new issue of shares, but from debt and internal accruals. Basically they had too much cash and insteadd of returning it to stockholders they simply threw it away

Nalin says:

You are right they might have overprovided depreciation. Do you want to base our presentation on that premise. Are you sure enough to make it a KEY assumption ?

Nalin says:

I'd rather just make it an additional upside

Sanjay says:

Not at all. What I want is to inform our investor group that this is classic case of massive misallocation of cash generated from operations. And that a rational person in control will have an opportunity to correct that misallocation and create value

Sanjay says:

Fine, you'can make it an additional upside but I should be in the document

Nalin says:

Okay - so we make that an upside that an acquirer gets - when he gains control. But I don't think we should ask him to pay for an upside - that we have no way of proving at this stage.

Nalin says:

Then the strategy remains more or less unchanged ?

Sanjay says:

Please also notice that my additional debt of Rs 100 cr requires an annual interest outgo of only Rs 15 cr and I have assumed c discretionary cash earnings of 45 cr p.a. at least until TUF benefits are available for the next three years. Even if the discretionary earnigns come to less than 45 cr, I can still pay a Rs 100 cr dividend financed out of from borrowed funds because the company is hugely

Sanjay says:

underleveraged.

Sanjay says:

Therefor I can bring my effecive cost of acqusition to Rs 18 cr for a 40% stake

Nalin says:

Like I said earlier - financial engineering is not something an acquirer will pay for up front

Sanjay says:

Why not? I would if I was certain of the benefits. If we get more info on the company's cash generating abilites then I would very gladly pay for financial engerring value

Nalin says:

In some cases it makes sense to go to the hilt in paying. In this case it makes sense to pay as little as possible - and not factor in too many upsides

Nalin says:

How do you get certain of the benefits ?

Sanjay says:

I agree with the conservatinve approach u are taking but putting a value equal to 100% of adjusted book value is too conservative, I feel.

Sanjay says:

We go to Coimbatore on a fact finding mission. we can control costs by travelling by train

Nalin says:

Its conservative - but in this case, paying more doesn't achieve much additional advantage - it disproportionately increases our downside risk. If we stick to market price in our bids - we have almost zero risk of loss - and a considerable upside.

Nalin says:

Even getting control of this company is very difficult - with labour, politics etc involved. Also, it probably has liabilities we haven't even dreamed off - such as corp guarantees for the steel project. Its a mess we don't want.

Sanjay says:

Ok think of it this way. Suppose, the amount of cash that can be taken out of this company without hurting it is only Rs 35 cr p.a. for the next three years and we are use a discolunt rate of 20% p.a. Then the present value of the next three year cash flows alone comes to Rs 650 per share.

Nalin says:

Its pure GM - with controlled downside risks

Sanjay says:

Nalin how can we do a successful GM when we are delaing with promoters who are not cash rich? I thought u did that cash rich promoters

Nalin says:

Listen - the way the industry is going - the company may need to get cash negative - to be able to emerge a strong player

Sanjay says:

But we'll be out well before that happens

Nalin says:

How do you get out ?

Sanjay says:

Leveraged recap can esnure that our cost is negligible. Then whatever we sell the company for is profit

Nalin says:

You can't do a leveraged re-cap if we fear uncertain cash flows - because of a recession + competition. Depending only on the TDF is not enough.

Sanjay says:

To quote u, "I agree to disagree!"

Nalin says:

But what strategy do we put in the book

Sanjay says:

I guess it would be best if we were to fix the meeting for wednesday and I come to mumbai on Monday and we spend 2 days on it

Sanjay says:

Im ust tell u that I am enjoying working with u

Nalin says:

Thats good.

Nalin says:

Lets give one last attempt at coming to consensus now.

Nalin says:

Tell me why is my strategy flawed. Let me defend it for a change.

Sanjay says:

It all comes down to valuation. You are being unlta conservative in valuing this company. A company that produces a cash profit of 70 cr cannot be worth less than the book value of 117 cr. This is true even if a large part of those earnings are not discretionary.

Nalin says:

I'm not saying its not worth more - I'm just saying we shouldn't pay more - what's wrong with sticking to a low price ?

Sanjay says:

Your views on valuation in the presentation are so pessimistic that the whole project will turn off investors

Sanjay says:

and I thought u were an investment banker!

Nalin says:

I WAS an investment banker. Now I think more like a value investor.

Nalin says:

My views on valuation were given on the next page - where I said that it could be worth Rs 1800

Nalin says:

Did you get the presentation ?

Sanjay says:

LOL! i agree we sohuld pay less if we can get away with it but how to achieve it is the issue here. We cannot do this deal unless we convince investors that this is a sitting duck

Nalin says:

But did you get the presentation - I hope you aren't refering only to my initial note

Sanjay says:

That 1800 is based on relative valuation with peers, something that may be difficut to sell to our investors.

Nalin says:

Before I proceed I need to know if you got the presentation

Sanjay says:

I got the presentation. Also, our strategy shoudl reflect the illiquidity of the stock for exit. We cannot sell a deal to investor on the basis that one of the exit routes will be thru the market when dailty volume is 15 shares. We cannot also tell them to hold it as a value stock. Our investors want to make a quick buck.

Nalin says:

I mentioned exit through the market only when the deal is on (and only to a very limited extent). I mentioned illiquidity when I said only 32,000 shares were traded last year.

Nalin says:

Holding on to the stock is a worst case scenario. I think we shouldn't proceed unless we have an investor who is willing to take that risk. Because its a real risk. I can think of no other approach which has a lower risk.

Sanjay says:

The stock is so illiquid that mkt operations after Public Annoucement will not be feasible. under such circumstances, why not have a conditional two-tiered tender offer which guarantees either control or exit thru tender in their counter offer?

Nalin says:

Let me think about this for a minute ?

Sanjay says:

Say a 7% toehold at 850, a 21% offer at 1500 subject to minumum level of acceptance of 20% with a lower offer price of 850 if shares tendered are less than 21%

Nalin says:

I think the problem again will be return on investment. We did this exercise in Taurus. The return on investment was just too low

Nalin says:

What should be the offer size ?

Sanjay says:

The toehold will cost only Rs 7 cr. A 21% offer will cost 38 cr., 50% of which or 19 cr will be cash escrow

Nalin says:

You are saying a 21% conditional offer, with 20% minimum acceptance ?

Sanjay says:

yes

Nalin says:

But in terms of risk - how is this different from what I said. You still run the risk of getting stuck with acceptances in your offer at Rs 850 ? But the downside is that return on investment goes for a toss. It was bad enough under my option at only 50% annualised.

Nalin says:

You also run the risk of actually getting 21% at Rs 1500

Nalin says:

Are you saying the only problem with my plan is that we won't get an investor willing to take the risk of a residuary holding at Rs 850 ?

Sanjay says:

I am unable to explain. Either we have to meet or I have prepare a note on bidding strategy explaining why I think that a conditional offer may make sense. The main reason is that a conditional offer is a hedge. But it imposes an ban on market purchases. But mkt purchases are not going to happen in any case in this stock/

Nalin says:

Okay - we'll discuss conditional offers later. Lets go back to why my plan is flawed ?

Sanjay says:

Look at pg 18. What if they don't buy us out? What if they go to instutions and get them to not tender to us because of lack of significant premium to market offer fro us. There are 100 shares. 13+21+33 (rieter,promoter,instutions) or 67 will not come. 20 shares are are missing. therefore 87 will not come. we already have say 7%. so we'll get only 6% if institutions do not tender.

Sanjay says:

they can simply ignore us and just get institutions to not tender.

Sanjay says:

so we end up with 13% at 850 and no control just apin in their necks

Sanjay says:

in order to get the institutions to tender we have to offer a significant premium to market otherwise they will have an excuse for not tendering. I saw this in Gesco case

Sanjay says:

If institutions do not tender and they don't make a counter offer we are fucked

Nalin says:

There is only a small chance that FIs will pre-agree not to tender. I think FIs will keep quiet about their intentions - therefore LIBRA will be forced to act. Also Rieter may want to ext. I don't think Libra will ignore us because they will not want to take any chances of losing control.

Nalin says:

But assuming this happens (its only a 2% chance) then our max downside is we are stuck with a 15% stake at 850. In other options there are worse risks.

Sanjay says:

In case of Gesco, the institutions made it very clear that they will not tender unless they got book value. In Gesco the book value was 54 and return on equity was less than 5%. So we told them that the stock is not worth book value because ROI is so poor. Thay told us to fuck off and come back with a 54 offer.

Sanjay says:

In LIBRA book value is 2000 even though a lot of it is water, but it does give a huge excuse to institutions to not tender. Also there is a history of this stock which at one tiem sold for Rs 10,000

Nalin says:

FIs will certainly want to put pressure on LIbra to give a better counter offer. They won't want to give them guaranteed comfort - and suggest they don't need to counter offer. Rieter will also want a higher counter offer - so there won't be any guarantees from that end eithre

Nalin says:

Anyway - we are talking about the same flaw - the chance (in my opinion small) of a residuary stake at Rs 850 ? Is there any other flaw ?

Sanjay says:

Precisely the point. In order to put this company in play we have to make institutions the sellers. Once we do that with our offer then our offer is the minimum they would get and they would demand higher from promoters or Rieter.

Sanjay says:

Unless we induce instutions to sell, we cannot succeed. becasue in any proxy contrest tyhey would side with management

Nalin says:

Okay - but we have to be careful not to introduce higher risks just to eliminate that risk - also be careful not to dilute returns too much. If you can come up with such a plan good. If we can't - we scrap this project.

Sanjay says:

My basic difference with you on this is that u are approaching it as a GM operation, whereas I am appraoching it as an acqusition prior to a leveraged recap, but which could also become a GM operation.

Sanjay says:

Hopefully it will be the later

Nalin says:

I strongly feel that we should not acquire this company - but stick to GM

Sanjay says:

But even if it turns out to be the former, I can do a recap to get my cost to negligible levels

Nalin says:

Do you want to discuss GM vs acquisition a little more ?

Sanjay says:

OK

Sanjay says:

Let's talk about promoters. GM is done with cash rich guys not poor ones

Sanjay says:

thesze guys are leveraging to creep up. OK, chola may be a white knight in which case our probability of GM is that much higher

Nalin says:

Overgeneralisations are dangerous. Every situation is different. In this case, we keep the cash required to buy us out low - so that they can actually buy us out - therefore a low bid

Sanjay says:

u do have a point there

Nalin says:

If Cholamandalam is appears as a white knight and gives a counter offer without buying us out - we lose - but hopefully without a loss.

Nalin says:

Also please note if we start a bidding match, Cholamandalam can still come in - in that case our losses would be even higher

Sanjay says:

now u're making sense

Sanjay says:

what 2 do?

Sanjay says:

OK, here;s a plan, we go with your presentation with John and ASit and see how they feel about it. Do u want to talk to Asit about Libra?

Sanjay says:

On pg 19 of your presentation u mention, "If promoters do not give counter offer - we become largest shareholder". I don't agree with this because we will not have significant tenders at a low price offer if institutions are not participating

Nalin says:

Listen I don't want to steamroll you into this. So you keep thinking. I'll keep working on the presentation. Overall, I think we should give both plans to Asit and John, just to show that we have more ideas where Taurus came from. On whether the plan is good or not - we can decide tomorrow

Nalin says:

Okay - I'll take care of that

Sanjay says:

Just think about this aspct

Nalin says:

Yes - this requires a lot of thinking - I agree

Nalin says:

Earlier when I said we should give both plans to Asit _ I meant both projects not both plans

Nalin says:

Someone has just sent me an email from gescocorp. Should I check and see ?

Sanjay says:

WHATTT????

Nalin says:

Wait I'm checking

Nalin says:

A friend of mine has just joined Gesco Corp. He's coming to visit tomorrow. How wierd.

Sanjay says:

Don't tell him about me!

Nalin says:

I have this feeling that destiny is just a game played for God's perverse amusement

Nalin says:

I won't.

Sanjay says:

I wanna live

Nalin says:

Okay.

Sanjay says:

ask him what's happening in the company

Nalin says:

Any more detailed comments on Libra - such as page 19 ?

Nalin says:

I'll work on another draft of the presentation and send it to you - in the meantime you think strategy. But hurry up with Taurus. Because I need to print the presentation today

Sanjay says:

OK Give me 2 hours on Taurus. I agree with most of your work there, just a few points I want to add/amend

Nalin says:

Okay talk to you later then ?

Sanjay says:

In libra disagreement is on valuation, and accoringly on strategy, but i see your point that a alow priced offer will enable the promoters to buy us out at a lower cost

Sanjay says:

Bye?

Nalin says:

It was a stimulating discussion anyway. Bye.

Sanjay says:

bye

SUBSEQUENT DEVELOPMENTS:

Sunday, October 22, 2006

Adventures of a Risk Arbitrageur- The Case of Matrix Laboratories

From: Sanjay Bakshi

Sent: Sun 22/10/2006 20:22

To: BFBV

Subject: Adventures of a Risk Arbitrageur

Dear Students,

Some time ago, I had told you about a deal on which I was working. This was the deal involving the acquisition of Matrix Laboratories by Mylan. I had, at that time said, that there are multiple ways of looking for opportunities in this deal. I had disclosed one such way to you. This involved taking a long position in the stock and simultaneously selling the shares expected to be received back (due to over-tendering) in the futures market. The second leg of that trade would have involved selling the surplus shares as and when received in the spot market and simultaneously squaring up the short futures position. These trades, if they had been initiated, soon after announcement of the deal, had an expected pre-tax, hedged return of more than 25% p.a. after considering trading and hedging costs. For details of this trade see the text of a note prepared by Ankur Jain, one of my colleagues, who is three years senior to you. The note is at the bottom of this mail.

Such returns are considered to be mouth-watering by many hedge fund managers primarily because of low correlation to overall market.

However, this very fact, attracts more capital in this game which makes returns in the strategy described above less attractive for new capital. That brings me to the second way of looking at this deal.

Given that (1) this is a large transaction involving a liquid stock; and (2) the stock is trading in futures market, it was clear to me that much capital will enter this trade. One way of validating this is to see what happened to the November futures contract, which was the relevant contract for hedging purposes in this deal (assuming no delays - wrong assumption - more about that later). A few days after the announcement of the deal, sure enough, the November futures contract started to trade below the spot price and the gap kept on increasing progressively and at one time reached more than Rs 15 per share. That is, the November futures were trading Rs 15 below the spot in September. Why would that happen? All of you know the mathematical relationship between spot and futures prices. Futures are supposed to trade a premium not discount to spot. Why were November futures trading at a discount to spot?

Well part of the answer is that too much money was chasing this deal. The strategy of buying shares in the spot market and selling them in the futures market for November delivery depressed the price of November contract for technical reasons. Such technical reasons often create very interesting anomalies for exploitation by the alert investors. Let me explain. (I am listening to Sarah Brightman as I type this - I love this girl's voice :) - so I am in the mood to share some of my secrets with you :)

Well this offer was to open on 20 October 2006 and close on 8 November 2006 and the surplus shares and money for shares accepted would have reached us by 23 November. This means that the November contract was the relevant contract because its settlement date was after 23 November. And that's exactly why the November contract went to discount to the spot price.

One of the key risks in risk arb is that of unexpected delays. Well, in this case a delay did take place. See the following news reported on 19th October.

http://www.business-standard.com/common/storypage.php?leftnm=lmnu1&subLeft=1&autono=262276&tab=r

What did the delay mean? Well in this case it means that the November contract was no longer the relevant contract for hedging because by the time the surplus shares would come back after the delay, it would be past the settlement date for the November contract (futures contracts are settled on the last Thursday of every month.) Now what that that imply?

If November is no longer the right contract for hedging then people who were selling November contracts for hedging would now have to shift to December. That required them to buy back the November contract which would create demand for this contract on the long side. Looked another way, there was no logic anymore for the November contract to trade at a discount to the spot price. So how does one make money in this? One way is to go long November contract and short December contract. Another way is to just go long November contract in the expectation that the discount will vanish.

And vanish it did- It HAD to didn't it? The market may be foolish for a while but it does not remain foolish forever. This window of opportunity was available for just a few hours - too little for the unaware investor -but just right for the alert one.

Total pre-tax realized return came to 15% flat on invested capital over just a few hours - the annualized returns need not be computed as they would look obscene :)

SB

P.S.: "The answer is out there, Neo, and it's looking for you, and it will find you if you want it to." - Trinity in "The Matrix"

Text of Note prepared on 6 September 2006

MATRIX LABS

On August 28, 2006, Mylan Labs announced the acquisition of 51.5% stake of Matrix Laboratories through a Share Purchase Agreement between Mylan (acquirer) and Mr N Prasad (Promoter of Matrix Labs) and the other Persons Acting in Concert.

The acquisition of 51.5% stake in the Indian company triggered the SEBI Takeover Code, 1997 which required the acquirer, Mylan Labs to come out with an open offer to buy at least 20% of the outstanding equity from the public shareholders of the acquired company, Matrix Labs. Also, post acquisition 5% of the outstanding shares are going to continue remain with Mr. N Prasad.

On August29, 2006, Mylan Labs came out with an open offer to buy 20% of the outstanding shares of the company from the public shareholders (except the parties to the Share Purchase Agreement).

Date of opening of offer: October 20, 2006

Date of closing of offer: November 08, 2006

Last date by which cash will be received: November 23, 2006

Investment Rationale

The excel sheet shows the shareholding pattern of the company. 51.5% has been acquired by Mylan. Also 5% is going to remain with Mr N Prasad. Thus, for the open offer of 20%, the % of eligible shares for tendering is (100-51.5-5) = 43.5%.

In our view, there might be some "brain dead" investors which in turn might increase the acceptance ratio during the open offer. Even if there are 3-4% investors who do not tender their shares during the open offer, the acceptance ratio will be 50%.

For 100 shares that we buy at Rs 274/ share, 50 might be accepted in the open offer at Rs 306/share and the rest 50 shares will be returned to us.

To hedge the risk of the price of the returned shares falling down, we can hedge our position using the availability of the Matrix Labs stock in the F & O Market.

The calculations have been taken for 6 F&O contracts because the deal will take 3 months and we will have to take 3 pairs of buy-sell.

The calculations show that for a fully hedged position in this trade, over a 78 day period ( Sep 07,2006- Nov 23, 2006) , the annualised returns after all costs of trading is close to 25.22%.

Sent: Sun 22/10/2006 20:22

To: BFBV

Subject: Adventures of a Risk Arbitrageur

Dear Students,

Some time ago, I had told you about a deal on which I was working. This was the deal involving the acquisition of Matrix Laboratories by Mylan. I had, at that time said, that there are multiple ways of looking for opportunities in this deal. I had disclosed one such way to you. This involved taking a long position in the stock and simultaneously selling the shares expected to be received back (due to over-tendering) in the futures market. The second leg of that trade would have involved selling the surplus shares as and when received in the spot market and simultaneously squaring up the short futures position. These trades, if they had been initiated, soon after announcement of the deal, had an expected pre-tax, hedged return of more than 25% p.a. after considering trading and hedging costs. For details of this trade see the text of a note prepared by Ankur Jain, one of my colleagues, who is three years senior to you. The note is at the bottom of this mail.

Such returns are considered to be mouth-watering by many hedge fund managers primarily because of low correlation to overall market.

However, this very fact, attracts more capital in this game which makes returns in the strategy described above less attractive for new capital. That brings me to the second way of looking at this deal.

Given that (1) this is a large transaction involving a liquid stock; and (2) the stock is trading in futures market, it was clear to me that much capital will enter this trade. One way of validating this is to see what happened to the November futures contract, which was the relevant contract for hedging purposes in this deal (assuming no delays - wrong assumption - more about that later). A few days after the announcement of the deal, sure enough, the November futures contract started to trade below the spot price and the gap kept on increasing progressively and at one time reached more than Rs 15 per share. That is, the November futures were trading Rs 15 below the spot in September. Why would that happen? All of you know the mathematical relationship between spot and futures prices. Futures are supposed to trade a premium not discount to spot. Why were November futures trading at a discount to spot?

Well part of the answer is that too much money was chasing this deal. The strategy of buying shares in the spot market and selling them in the futures market for November delivery depressed the price of November contract for technical reasons. Such technical reasons often create very interesting anomalies for exploitation by the alert investors. Let me explain. (I am listening to Sarah Brightman as I type this - I love this girl's voice :) - so I am in the mood to share some of my secrets with you :)

Well this offer was to open on 20 October 2006 and close on 8 November 2006 and the surplus shares and money for shares accepted would have reached us by 23 November. This means that the November contract was the relevant contract because its settlement date was after 23 November. And that's exactly why the November contract went to discount to the spot price.

One of the key risks in risk arb is that of unexpected delays. Well, in this case a delay did take place. See the following news reported on 19th October.

http://www.business-standard.com/common/storypage.php?leftnm=lmnu1&subLeft=1&autono=262276&tab=r

What did the delay mean? Well in this case it means that the November contract was no longer the relevant contract for hedging because by the time the surplus shares would come back after the delay, it would be past the settlement date for the November contract (futures contracts are settled on the last Thursday of every month.) Now what that that imply?

If November is no longer the right contract for hedging then people who were selling November contracts for hedging would now have to shift to December. That required them to buy back the November contract which would create demand for this contract on the long side. Looked another way, there was no logic anymore for the November contract to trade at a discount to the spot price. So how does one make money in this? One way is to go long November contract and short December contract. Another way is to just go long November contract in the expectation that the discount will vanish.

And vanish it did- It HAD to didn't it? The market may be foolish for a while but it does not remain foolish forever. This window of opportunity was available for just a few hours - too little for the unaware investor -but just right for the alert one.

Total pre-tax realized return came to 15% flat on invested capital over just a few hours - the annualized returns need not be computed as they would look obscene :)

SB

P.S.: "The answer is out there, Neo, and it's looking for you, and it will find you if you want it to." - Trinity in "The Matrix"

Text of Note prepared on 6 September 2006

MATRIX LABS

On August 28, 2006, Mylan Labs announced the acquisition of 51.5% stake of Matrix Laboratories through a Share Purchase Agreement between Mylan (acquirer) and Mr N Prasad (Promoter of Matrix Labs) and the other Persons Acting in Concert.

The acquisition of 51.5% stake in the Indian company triggered the SEBI Takeover Code, 1997 which required the acquirer, Mylan Labs to come out with an open offer to buy at least 20% of the outstanding equity from the public shareholders of the acquired company, Matrix Labs. Also, post acquisition 5% of the outstanding shares are going to continue remain with Mr. N Prasad.

On August29, 2006, Mylan Labs came out with an open offer to buy 20% of the outstanding shares of the company from the public shareholders (except the parties to the Share Purchase Agreement).

Date of opening of offer: October 20, 2006

Date of closing of offer: November 08, 2006

Last date by which cash will be received: November 23, 2006

Investment Rationale

The excel sheet shows the shareholding pattern of the company. 51.5% has been acquired by Mylan. Also 5% is going to remain with Mr N Prasad. Thus, for the open offer of 20%, the % of eligible shares for tendering is (100-51.5-5) = 43.5%.

In our view, there might be some "brain dead" investors which in turn might increase the acceptance ratio during the open offer. Even if there are 3-4% investors who do not tender their shares during the open offer, the acceptance ratio will be 50%.

For 100 shares that we buy at Rs 274/ share, 50 might be accepted in the open offer at Rs 306/share and the rest 50 shares will be returned to us.

To hedge the risk of the price of the returned shares falling down, we can hedge our position using the availability of the Matrix Labs stock in the F & O Market.

The calculations have been taken for 6 F&O contracts because the deal will take 3 months and we will have to take 3 pairs of buy-sell.

The calculations show that for a fully hedged position in this trade, over a 78 day period ( Sep 07,2006- Nov 23, 2006) , the annualised returns after all costs of trading is close to 25.22%.

Saturday, July 08, 2006

The Case of Neyveli Lignite

The meeting’s agenda was to discuss the central government’s plans to sell 10% of the shares of

The Prime Minister had invited the CM to consult him on various issues related to the plan. A consultation paper had been forwarded to the CM prior to the meeting. The CM was totally opposed to the idea of selling shares in Neyveli. He became very upset after reading the consultation paper and was intending to deliver a “take it or leave it” threat to the PM in the meeting. The PM, a wise man, was quite aware of the hostile reaction he was likely to receive from the CM.

The PM was prepared…

Date:

PM (standing up and welcoming the CM into his room and pointing him to a sofa): Ah, welcome sir, please be seated here. I will be with you in just a moment.

Most importantly, post leveraged recapitalization, Neyveli will remain a very strong company in which the government will continue to hold 93.56% stake. And its other shareholders will benefit too by receiving a substantial amount of cash and a fairer market price for their shares in the stock market.

CM: Ok. So market value is important. Tell me how your plan will work.

At current interest rates of about 10% p.a., the annual cost of debt will come to Rs 3 billion. And during the last five years, the company has generated cash of more than Rs 15 billion per annum. Putting a debt of Rs 30 billion on the balance sheet of Neyveli will not jeopardize the company’s solvency or its future growth plans because of its ability to generate cash of about 5 times its annual interest requirements. Indeed, I am told, that should Neyveli raise this debt, it will enjoy a very high credit rating.

Now let’s see we already have Rs 40 billion in net cash. The company borrowes an additional Rs 30 billion by selling 10% bonds. That makes it Rs 70 billion of cash. Of this, I propose to distribute Rs 5 billion to the workers of the Neyveli in appreciation of their contribution to the company. Neyveli has 19,000 workers. Each of them will receive for his/her valuable contribution, one years’ salary as bonus out of the money raised by the company.

Thank you sir! I have taken the liberty to draw up the draft press release of the “Karunanidhi Plan”. Let’s sit here and read it together and see if we need to make any changes.

Draft Press Release

Jointly issued by the office of the Chief Minister of Tamil Nadu and the office of the Prime Minister of India

- There shall be no sale of the company’s shares by the central government.

- The company shall, against the security of its assets and cash flow, borrow Rs 30 billion.

- After the completion of the borrowing, the company shall distribute a sum of Rs 5 billion to all the 19,000 workers in proportion of their existing wages, as special bonus for their valuable services to the company and the nation.

- After the payment of the special bonus, the company shall pay its stockholders, a special dividend of Rs 65 billion. Since the government of

- The central government has undertaken that out of Rs 60 billion it expects to receive as dividend, it will spend at least Rs 20 billion towards the development of infrastructure of Tamil Nadu.

The Chief Minister commented: “I am grateful to the Prime Minister to endorse my plan for the transformation of financing the government’s deficits. My plan fully ensures that the ownership pattern of profitable, public sector companies does not change, that the employment at such companies remains unchanged, that workers are rewarded suitably for their valuable contribution to their company, and the central government can raise substantial resources, a significant part of which shall be allocated to the development of this state.”

Sunday, April 30, 2006

Sunday, April 02, 2006

Nothing Ventured, Something Gained: The Titan Industries Special Situation

On August 31, 2005, Titan Industries made the following announcement to the exchanges:

Titan Industries Ltd. has informed the Exchange that at the meeting of BODs of the company held on August 31,2005, the directors have approved the issue of Partly Convertible Debentures(PCDs) of Rs.600 each on a rights basis in the ratio of one PCD for every twenty equity shares held in the company to the shareholders of the company as on a record date to be fixed by the board or by a duly constituted committee thereof. The duly constituted committee of the board for the Rights Issue will also decide on matters incidental to the Issue. The PCD will comprise of:a)Part 'A' will be converted into one equity share(Face value of Rs.10/-) in a price band of Rs.325/- to Rs.375/- which shall be fixed closer to the record date by the BODs of the company.b)Part 'B' will be one Non-Convertible Debenture(NCD),of the face value of the balance amount out of the Rs.600/- on due appropriation of the amount of equity shares priced as per 'a' above. The NCDs will be carrying a coupon rate of 6.75% per annum payable annually and redeemable at the end of 5 years. The total issue size is calculated to be around Rs.126.83 crores comprising of 21,13,813 PCDs of Rs.600 each.

On December 26, 2005, another announcement was made by the company: