Sunday, April 30, 2006

Sunday, April 02, 2006

Nothing Ventured, Something Gained: The Titan Industries Special Situation

On August 31, 2005, Titan Industries made the following announcement to the exchanges:

Titan Industries Ltd. has informed the Exchange that at the meeting of BODs of the company held on August 31,2005, the directors have approved the issue of Partly Convertible Debentures(PCDs) of Rs.600 each on a rights basis in the ratio of one PCD for every twenty equity shares held in the company to the shareholders of the company as on a record date to be fixed by the board or by a duly constituted committee thereof. The duly constituted committee of the board for the Rights Issue will also decide on matters incidental to the Issue. The PCD will comprise of:a)Part 'A' will be converted into one equity share(Face value of Rs.10/-) in a price band of Rs.325/- to Rs.375/- which shall be fixed closer to the record date by the BODs of the company.b)Part 'B' will be one Non-Convertible Debenture(NCD),of the face value of the balance amount out of the Rs.600/- on due appropriation of the amount of equity shares priced as per 'a' above. The NCDs will be carrying a coupon rate of 6.75% per annum payable annually and redeemable at the end of 5 years. The total issue size is calculated to be around Rs.126.83 crores comprising of 21,13,813 PCDs of Rs.600 each.

On December 26, 2005, another announcement was made by the company:

Titan Industries Ltd. has informed the Exchange that at the 'Rights Issue Committee Meeting' of the Board held on December 26, 2005, the Members after deliberations on the subject have finalised the price of the equity shares comprised in the Partly Convertible Debentures (PCD) (forming Part A of the PCD) to be issued on allotment, at Rs.350 per equity share of a face of Rs.10 per share and inclusive of premium of Rs.340 per equity share and within the price band of Rs.325 - Rs 375 per equity share, as approved by the Board in their earlier Meeting. The price of the Non-Convertible Debenture (NCD) comprised in Part B has been fixed at Rs.250 per NCD carrying an annual interest of 6.75% p.a. and redeemable at par at the end of 5 years from the date of allotment.

On January 3, 2006, the company filed the draft offer document with the Securities and Exchange Board of India (SEBI).

On February 3, 2006, the company fixed March 06, 2006 as the record date for the purpose of the rights issue.

One of the key aspects of the offer was the buyback arrangement made by the company for the Part B of the PCD. Called the "Khokha buyback scheme" (see page 288 of the offer document), the applications had the option to sell the Part B of the PCD, having a face value of Rs 250, at a small discount.

Given that the stock price of the company was around Rs 800 per share, this looked like a very interesting idea. The investment operation would have involved buying 20 shares at Rs 800 on cum-rights basis, selling all of them ex-rights basis, and acquiring a the right to subscribe for the PCD at a low, or zero cost. The reasoning was that given the low dilution, the market would virtually ignore the dilution factor. Moreover, once the Rs 600 PCD was bought, a sum of slightly less than Rs 250 could be recovered by opting for the Khokha buyback scheme. In effect, the operation, if successful would have resulted in the acquisition of one share of this company at a price slightly more than Rs 350, even though its prevailing market price was Rs 800.

Not bad, eh?

Even more interesting was the fact that Titan stock was traded in futures and options segment. This meant that it was possible to buy 20 shares in the spot market on cum-rights basis and sell 21 shares in the futures market on ex-rights basis, locking in a handsome profit. However, the NSE decided make the necessary adjustments for the rights issue in the outstanding futures and options contracts. See this notice, and this one and this one.

So what happened exactly?

On 24 February - the last date on which the stock traded on a cum-rights basis, Titan stock closed at Rs 799 and had an average price of Rs 792 for that day. So one could easily have bought 20 shares @ Rs 792 costing a total of Rs 15,840.

On 27 February - the first date on which the stock traded on ex-rights basis, Titan stock closed at Rs 780 and had an average price of Rs 785. However, by March 1 the price had increased to Rs 792 which was the same as the cum-rights price. The market had, as expected, ignored the dilution.

I did not do this transaction though. Why? There were several reasons.

One was the capital intensity of the operation. The maximum spread, ignoring all costs, was Rs 442 (Rs 792 less Rs 350 effective cost of one new equity share). To get this gross maximum spread, one had to invest Rs 15,840 initially which was 35 times the gross maximum spread.

The second reason was to do with costs. In order to get one rights share, one had to buy and sell 20 equity shares in the spot market. In addition, the operation would have involved selling 21 shares in the futures market, and then squaring up that position later. The transaction costs of doing business in the spot market for 20 shares, and the futures market for 21 shares, must be loaded on to the cost of the one share to be acquired in the rights issue. Simple calculation showed that once when this was factored in the gross spread of Rs 442 was reduced very substantially. This made the operation less profitable and even more capital intensive than before.

In risk arbitrage, transaction costs matter - they matter a lot.

The third reason killed it. To generate the capital to do the deal would have involved substantial sales of the existing portfolio, resulting in significant taxes, which should correctly be counted as the cost of this operation.

All in all, nothing was ventured, but something was gained - knowledge - and that's what I am sharing here with you tonight...

Titan Industries Ltd. has informed the Exchange that at the meeting of BODs of the company held on August 31,2005, the directors have approved the issue of Partly Convertible Debentures(PCDs) of Rs.600 each on a rights basis in the ratio of one PCD for every twenty equity shares held in the company to the shareholders of the company as on a record date to be fixed by the board or by a duly constituted committee thereof. The duly constituted committee of the board for the Rights Issue will also decide on matters incidental to the Issue. The PCD will comprise of:a)Part 'A' will be converted into one equity share(Face value of Rs.10/-) in a price band of Rs.325/- to Rs.375/- which shall be fixed closer to the record date by the BODs of the company.b)Part 'B' will be one Non-Convertible Debenture(NCD),of the face value of the balance amount out of the Rs.600/- on due appropriation of the amount of equity shares priced as per 'a' above. The NCDs will be carrying a coupon rate of 6.75% per annum payable annually and redeemable at the end of 5 years. The total issue size is calculated to be around Rs.126.83 crores comprising of 21,13,813 PCDs of Rs.600 each.

On December 26, 2005, another announcement was made by the company:

Titan Industries Ltd. has informed the Exchange that at the 'Rights Issue Committee Meeting' of the Board held on December 26, 2005, the Members after deliberations on the subject have finalised the price of the equity shares comprised in the Partly Convertible Debentures (PCD) (forming Part A of the PCD) to be issued on allotment, at Rs.350 per equity share of a face of Rs.10 per share and inclusive of premium of Rs.340 per equity share and within the price band of Rs.325 - Rs 375 per equity share, as approved by the Board in their earlier Meeting. The price of the Non-Convertible Debenture (NCD) comprised in Part B has been fixed at Rs.250 per NCD carrying an annual interest of 6.75% p.a. and redeemable at par at the end of 5 years from the date of allotment.

On January 3, 2006, the company filed the draft offer document with the Securities and Exchange Board of India (SEBI).

On February 3, 2006, the company fixed March 06, 2006 as the record date for the purpose of the rights issue.

One of the key aspects of the offer was the buyback arrangement made by the company for the Part B of the PCD. Called the "Khokha buyback scheme" (see page 288 of the offer document), the applications had the option to sell the Part B of the PCD, having a face value of Rs 250, at a small discount.

Given that the stock price of the company was around Rs 800 per share, this looked like a very interesting idea. The investment operation would have involved buying 20 shares at Rs 800 on cum-rights basis, selling all of them ex-rights basis, and acquiring a the right to subscribe for the PCD at a low, or zero cost. The reasoning was that given the low dilution, the market would virtually ignore the dilution factor. Moreover, once the Rs 600 PCD was bought, a sum of slightly less than Rs 250 could be recovered by opting for the Khokha buyback scheme. In effect, the operation, if successful would have resulted in the acquisition of one share of this company at a price slightly more than Rs 350, even though its prevailing market price was Rs 800.

Not bad, eh?

Even more interesting was the fact that Titan stock was traded in futures and options segment. This meant that it was possible to buy 20 shares in the spot market on cum-rights basis and sell 21 shares in the futures market on ex-rights basis, locking in a handsome profit. However, the NSE decided make the necessary adjustments for the rights issue in the outstanding futures and options contracts. See this notice, and this one and this one.

So what happened exactly?

On 24 February - the last date on which the stock traded on a cum-rights basis, Titan stock closed at Rs 799 and had an average price of Rs 792 for that day. So one could easily have bought 20 shares @ Rs 792 costing a total of Rs 15,840.

On 27 February - the first date on which the stock traded on ex-rights basis, Titan stock closed at Rs 780 and had an average price of Rs 785. However, by March 1 the price had increased to Rs 792 which was the same as the cum-rights price. The market had, as expected, ignored the dilution.

I did not do this transaction though. Why? There were several reasons.

One was the capital intensity of the operation. The maximum spread, ignoring all costs, was Rs 442 (Rs 792 less Rs 350 effective cost of one new equity share). To get this gross maximum spread, one had to invest Rs 15,840 initially which was 35 times the gross maximum spread.

The second reason was to do with costs. In order to get one rights share, one had to buy and sell 20 equity shares in the spot market. In addition, the operation would have involved selling 21 shares in the futures market, and then squaring up that position later. The transaction costs of doing business in the spot market for 20 shares, and the futures market for 21 shares, must be loaded on to the cost of the one share to be acquired in the rights issue. Simple calculation showed that once when this was factored in the gross spread of Rs 442 was reduced very substantially. This made the operation less profitable and even more capital intensive than before.

In risk arbitrage, transaction costs matter - they matter a lot.

The third reason killed it. To generate the capital to do the deal would have involved substantial sales of the existing portfolio, resulting in significant taxes, which should correctly be counted as the cost of this operation.

All in all, nothing was ventured, but something was gained - knowledge - and that's what I am sharing here with you tonight...

Creating Free Warrants: The Case of JSW Steel

On January 20, 2006, JSW Steel gave the following notice to the exchanges:

JSW Steel Limited has informed the Exchange that the Board at its meeting held on Jaunary 20,2006 has pursuant to section 81(1) of the Companies Act, 1956 has approved the issue of Equity Shares with Warrants on Rights basis to the existing shareholders of the Company. The total amount proposed to be raised by Rights issue of equity shares (excluding the amount of equity issue pursuant to conversion of warrants) shall not exceed a sum of Rs. 400 crores. The said Rights issue proceeds shall be utilized for part financing the Cold Rolling Mill Project of one million tpa capacity proposed to be set up at the Company's manufacturing unit at Village Toranagallu, Bellary Dist, Karnataka at an estimated project cost of Rs. 1000 crores. The principal terms and conditions governing the issue of equity shares with warrants on rights basis are as under: The equity shares and warrants will be offered for subscription for cash on a record date (to be decided later) as under: (a) (1) Equity shares for every (8) Equity Shares held as on the Record Date and (1) Series A and (1) Series B Warrants for every fully paid up Equity Share being subscribed and allotted on Rights basis under this issue. (b) Each equity share shall be offered at a price to be determined (including the warrant conversion price) later by a Committee of Directors formed for this purpose. (c) Each warrant will entitle the holder thereof to apply for 1 (one) equity share of Rs. 10/- each at a price and on terms set forth below (i) Warrant Conversion Period for Series A Warrants shall be the period commencing after 18months from the Date of Allotment upto 36 months from the Date of Allotment. The Warrant Conversion Period for Series B Warrants shall be the period commencing after 24 months from the Date of Allotment upto 48 months from the Date of Allotment.

On January 30, 2006, the company filed the draft offer document with Securities and Exchange Board of India (SEBI) for the rights issue.

On February 27, 2006, the stock price of JSW Steel closed at Rs 203.55. That's the date on which I wrote a note on a potential opportunity to acquire free warrants in the company.

Given that the current stock price of JSW Steel is Rs 303 per share, and the expected terms of the forthcoming rights issue, its now quite likely that the warrants would be free for investors who bought on or around the date of the note.

Here is the text of the note:

JSW Steel Limited is planning a rights issue. Depending on the exact terms of the issue, we believe there may be a lucrative opportunity to acquire a zero-cost, or very low-cost, long-term warrants in this company.

When a company wishes to issue new shares to raise equity capital, it has to first offer them proportionately to its current shareholders. This “pre-emptive right” is granted to shareholders of all Indian companies by law. If the company wishes to issue shares to a different body of shareholders than its existing shareholders, this law requires the company to take prior approval from its current shareholders to waive off their pre-emptive right.

Obviously, like all options, this pre-emptive right to buy shares has value. So, when warrants are issued by a company, that action takes away the value of this pre-emptive right and transfers it to a separate certificate. Therefore, the value of the shares before issue of the warrants must equal the sum of (1) the value of the shares after such issue; and (2) the value of the warrants. At least that’s what the theory says.

Well, in practice, things don’t work out as the theory says. That’s because the theory assumes that markets are efficient and there is no difference between price and value. But the reality is quite different. Price and value often diverge by a large margin. And when value of a stock exceeds its price, the act of separating something valuable from that stock typically does not result in a compensating reduction in its price after the separation.

In the context of warrants this means that when the stock is cheap, the package of stock and warrants will tend to command a better price in the market than would the stock alone. This means that, under certain circumstances, it is possible to buy shares on cum basis, and sell them on ex basis at a price which implies acquisition of warrants at zero cost, or very low cost.

Before we return to warrants, however, we would offer two more applications of the above rule which we have profitably employed in the past. We want to do this to demonstrate the practical utility of the rule.

Dividend stripping

Cheap stocks often offer high dividend yields. If dividend cover is sufficient and its highly likely that the past dividend will be continued, then it’s possible to buy the stock on cum-dividend basis, and subsequently sell it on an ex-dividend basis at the same price, and strip the dividend for free. This approach has worked in spades in the past. The package of dividend plus ex-dividend stock price is worth more than the stock price before dividend.

JSW Steel Limited has informed the Exchange that the Board at its meeting held on Jaunary 20,2006 has pursuant to section 81(1) of the Companies Act, 1956 has approved the issue of Equity Shares with Warrants on Rights basis to the existing shareholders of the Company. The total amount proposed to be raised by Rights issue of equity shares (excluding the amount of equity issue pursuant to conversion of warrants) shall not exceed a sum of Rs. 400 crores. The said Rights issue proceeds shall be utilized for part financing the Cold Rolling Mill Project of one million tpa capacity proposed to be set up at the Company's manufacturing unit at Village Toranagallu, Bellary Dist, Karnataka at an estimated project cost of Rs. 1000 crores. The principal terms and conditions governing the issue of equity shares with warrants on rights basis are as under: The equity shares and warrants will be offered for subscription for cash on a record date (to be decided later) as under: (a) (1) Equity shares for every (8) Equity Shares held as on the Record Date and (1) Series A and (1) Series B Warrants for every fully paid up Equity Share being subscribed and allotted on Rights basis under this issue. (b) Each equity share shall be offered at a price to be determined (including the warrant conversion price) later by a Committee of Directors formed for this purpose. (c) Each warrant will entitle the holder thereof to apply for 1 (one) equity share of Rs. 10/- each at a price and on terms set forth below (i) Warrant Conversion Period for Series A Warrants shall be the period commencing after 18months from the Date of Allotment upto 36 months from the Date of Allotment. The Warrant Conversion Period for Series B Warrants shall be the period commencing after 24 months from the Date of Allotment upto 48 months from the Date of Allotment.

On January 30, 2006, the company filed the draft offer document with Securities and Exchange Board of India (SEBI) for the rights issue.

On February 27, 2006, the stock price of JSW Steel closed at Rs 203.55. That's the date on which I wrote a note on a potential opportunity to acquire free warrants in the company.

Given that the current stock price of JSW Steel is Rs 303 per share, and the expected terms of the forthcoming rights issue, its now quite likely that the warrants would be free for investors who bought on or around the date of the note.

Here is the text of the note:

Note on JSW Steel Opportunity

By Sanjay Bakshi

February 27, 2006

By Sanjay Bakshi

February 27, 2006

JSW Steel Limited is planning a rights issue. Depending on the exact terms of the issue, we believe there may be a lucrative opportunity to acquire a zero-cost, or very low-cost, long-term warrants in this company.

When a company wishes to issue new shares to raise equity capital, it has to first offer them proportionately to its current shareholders. This “pre-emptive right” is granted to shareholders of all Indian companies by law. If the company wishes to issue shares to a different body of shareholders than its existing shareholders, this law requires the company to take prior approval from its current shareholders to waive off their pre-emptive right.

Obviously, like all options, this pre-emptive right to buy shares has value. So, when warrants are issued by a company, that action takes away the value of this pre-emptive right and transfers it to a separate certificate. Therefore, the value of the shares before issue of the warrants must equal the sum of (1) the value of the shares after such issue; and (2) the value of the warrants. At least that’s what the theory says.

Well, in practice, things don’t work out as the theory says. That’s because the theory assumes that markets are efficient and there is no difference between price and value. But the reality is quite different. Price and value often diverge by a large margin. And when value of a stock exceeds its price, the act of separating something valuable from that stock typically does not result in a compensating reduction in its price after the separation.

In the context of warrants this means that when the stock is cheap, the package of stock and warrants will tend to command a better price in the market than would the stock alone. This means that, under certain circumstances, it is possible to buy shares on cum basis, and sell them on ex basis at a price which implies acquisition of warrants at zero cost, or very low cost.

Before we return to warrants, however, we would offer two more applications of the above rule which we have profitably employed in the past. We want to do this to demonstrate the practical utility of the rule.

Dividend stripping

Cheap stocks often offer high dividend yields. If dividend cover is sufficient and its highly likely that the past dividend will be continued, then it’s possible to buy the stock on cum-dividend basis, and subsequently sell it on an ex-dividend basis at the same price, and strip the dividend for free. This approach has worked in spades in the past. The package of dividend plus ex-dividend stock price is worth more than the stock price before dividend.

Spin offs

When a cheap conglomerate company spins off a business division, then it is often possible to buy the stock of the conglomerate on a cum-deal basis, and subsequently sell it on an ex-deal basis, and get the shares of the newco for free, or almost free. There are plenty of examples of this working in the past. The package of newco and oldco shares commands a better price than the price of oldco alone.

JSW Steel Opportunity

JSW Steel Opportunity

This company is planning to raise a maximum of Rs 4 billion by offering shares to its existing shareholders. For every 8 shares held in the company, 1 share will be offered to the current shareholders at a price which is yet to be determined. And for every share subscribed, the company will allot 2 warrants. One of these warrants could be converted into one equity share 18 to 36 months from allotment. The other warrant could be converted into one equity share 24 to 48 months from allotment. The conversion price for both warrants will be at a discount to the stock price prevailing at the time of conversion. The extent of discount is yet to be determined. The warrants are adequately protected from corporate actions like stock splits, bonus issues, and further equity dilution. Moreover, the warrants shall be listed for trading soon after they have been allotted.

The exact terms of the right issue – in particular the price at which one share will be offered for every eight shares held, and the exact discount for pricing of warrants, will be announced shortly. Of the two, it’s the discount for pricing the warrants which is very important for the profitability of this operation. We expect the discount to be a minimum of 15%.

Assuming a discount of 15% and a stock price of Rs 300 at the time of conversion of the warrants (which is about 31 months from date of issue), the expected present value of two warrants allotted for every eight shares acquired comes to Rs 60 (assuming an opportunity cost of 15% p.a.).

The operation will involve the act of buying eight shares at Rs 205 on a cum-deal basis, selling nine shares on an ex-deal basis, at cost, and ending up owning the warrants for nothing. The basic assumption is that when the stock trades on ex-rights basis, the market would ignore the dilution factor caused by warrants. That is, nine shares in the company (eight bought from the market and one directly from the company) would sell for their cost, and two warrants would come for free. The reasoning behind this assumption has already been stated above. Specifically in this case, we expect the market to ignore the dilution factor due to warrants because of the following reasons:

- The underlying stock is ultra-cheap and the principle (when value of a stock exceeds its price, the act of separating something valuable from that stock typically does not result in a compensating reduction in its price after the separation) stated earlier is applicable.

- The warrants are of a long duration and uncertain subscription price.

- Only two warrants will be issued for every nine shares, so the extent of dilution is relatively small.

- If the stock price on ex-rights basis takes into account the value of the warrants also, then the stock will become ultra-cheap relative to current earning power, which will induce buying.

There are two ways this opportunity can be exploited. One would be from a pure arbitrage point of view. The other would be from an arbitrage plus straight equity viewpoint.

From the straight-equity-plus-arbitrage viewpoint, our recommendation is to buy the stock now. This will allow us to participate in the possible run-up of the stock price just before the stock turns ex-rights. Of course, this strategy also exposes us to market risk, which we believe, is worth taking in this case, given the inherent cheapness of the stock. If we are willing to take a market risk of about one month, then not only do we have a good change of getting the warrants for nothing, we are also likely to end up with a handsome profit on the straight equity component of the operation.

From a pure arbitrage viewpoint, we should buy just before the stock trades on ex-rights basis and sell it just after it turns ex-rights. Under this strategy, our intention will be to basically acquire the warrants at a zero-cost, or low cost basis. The chief advantage of the pure arbitrage approach over the other approach is that even in the worst case scenario i.e. even if the warrant dilution factor is factored in the pricing of stock on ex-rights basis, its hard to lose money.

This is just a preliminary note which will be updated as soon as the pricing information about the stock and warrants becomes available.

Reflections on Indian Stock Market Levels Revisited

John Galbraith once famously said:

"There are two classes of forecasters. Those who don’t know and those who don’t know they don’t know."

"There are two classes of forecasters. Those who don’t know and those who don’t know they don’t know."

“Stocks are high, they look high, but they're not as high as they look.”

During the eight months that elapsed since I wrote that blog, Nifty rocketed upwards and on

That’s a rise of 47% in eight months.

The obvious question that I am being asked now is: “What do you feel now about where the Indian stock market is headed?”

Still believing that I belong to the former class of Galbraith’s forecasters, my answer is: I don’t know.

Not knowing what lies ahead does not have to result in paralysis, however. So let me go out on a limb and give my views on the current state of the Indian stock market, and their implications for investment policy.

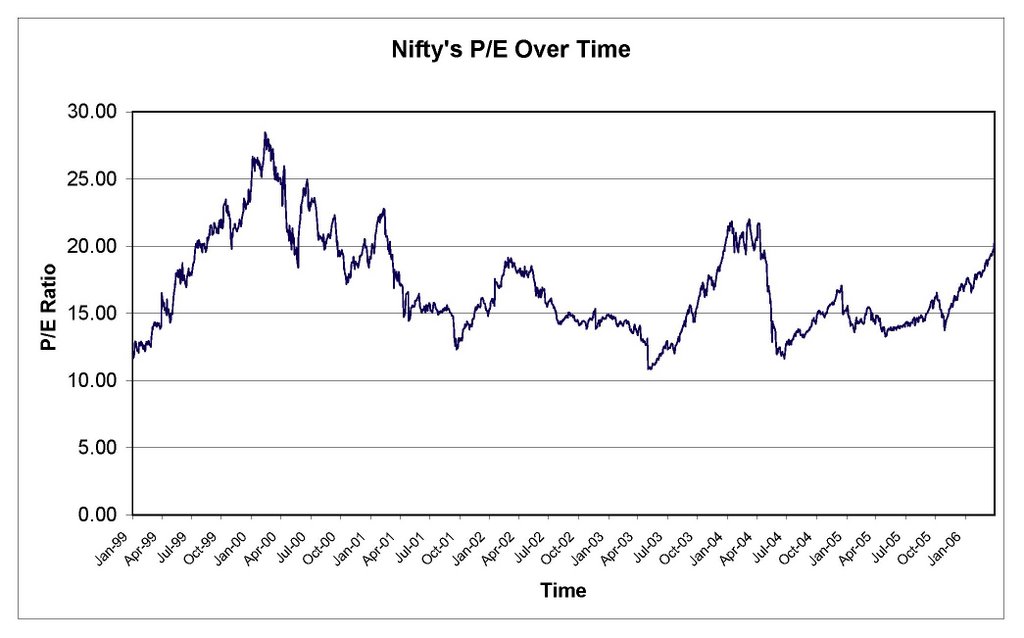

The chart below traces Nifty’s P/E multiple over time. On

Here is another chart which portrays an even bleaker picture (for bulls). This one traces Nifty’s Price-to-book value ratio over time.

On

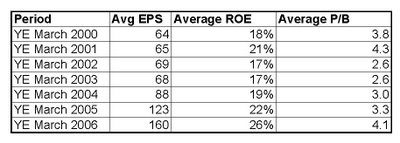

A simple look at the P/B ratio chart can easily lead one to conclude that Indian stock market levels are expensive, in comparison to the past. However, one must also see how well corporate

The table clearly shows that the rise in the P/B value is justified because corporate

The future, in other words, is uncertain.

Given this uncertainty, what is one to do? Here are some preliminary conclusions about investment policy going forward:

- Invest in companies that are significantly cheaper than the Nifty stocks.

- Identify stocks which are much more expensive than Nifty – for shorting. This will be necessary and desirable to protect the long positions in deep-value shares in the event of a market decline.

- Don’t leverage for straight equity investing (this was ok when markets collapsed in May 2004 – they have risen by 150% since then) but doing so in special situations is ok provided market risk is minimal.

- Allocate more capital towards special situations – probably 50% and keep the rest in deep-value shares.

Subscribe to:

Comments (Atom)