A few months ago, in August 2007, Mary Meeker, Morgan Stanley’s famous internet analyst published a bullish report on Google.

Google had just announced that its video web site, YouTube, would soon begin displaying video ads. In her report, Mary initially projected that YouTube’s video ads would result in incremental revenues of $720 million next year. But, while doing the number crunching for her report, Mary made a serious mistake. She took the price of the ads as “$20 CPM” to mean price per ad impression, and not per thousand ad impressions, which is what “CPM” means. In other words, she overstated projected revenues by a factor of 1,000. The actual projected incremental revenues, based on Mary’s corrected model were only $720,000, an insignificant number when compared with Google’s total revenues.

What’s interesting for us, however, is to observe what happened next. When Henry Blodget, another famous internet stock analyst, pointed out Mary’s mistake, on a public forum, she acknowledged her error.

However, instead of revising her overoptimistic conclusions, Mary left them intact! She rationalized them by revising yet another assumption in her model which resulted in much higher projected revenues for Google than would have been the case, had she not made this second revision, In her report update, Mary wrote: “In fixing the error, we also took the opportunity to dig deeper into our assumptions and.... we provide an updated scenario analysis of the opportunity.”

Mary Meeker’s response was not quite contrary to what most of us do, when we are presented with evidence which proves that our previous conclusions may be wrong. When we face such situations, our first reaction, almost always, is to discredit the new piece of evidence which proves us wrong. If we can’t do that, for example when the evidence is solid, we tend to invent other, new reasons, which would keep our prior conclusions intact.

Consider how a chain smoker, who smokes two packs of cigarettes a day behaves when he is first informed by his doctor that smoking causes lung cancer.

His first reaction is that of extreme discomfort arising out of two inconsistent pieces of information - that he smokes and that he was just informed by his doctor that smoking causes lung cancer. The chain-smoker, could, of course, eliminate the feeling of discomfort by quitting smoking immediately, but we know that is not going to be easy at all. Even the great Mark Twain, tried to give up smoking, and after having failed, once remarked, “Its not difficult to quit smoking, I’ve done it hundreds of times!”

One option before our chain smoking friend is to first discredit the medical evidence linking smoking and lung cancer. He could do that by questioning the validity of the medical research behind that finding, or, perhaps, by citing a silly the fact that he once knew a chain-smoking man who lived to a hundred years. Or, he will find other reasons for convincing himself that smoking isn’t really harmful, or that it helps him relax, prevents him from gaining weight etc.

The above example shows that we are capable of going to extremes in order to fool ourselves into believing that we’re right about things about which we are really wrong.

Contrary to the belief of most economic theorists, we’re really not rational animals. Rather, we are rationalizing ones. There are obvious lessons here for the readers.

Take the idea behind what is called as the “sunk-cost fallacy.” We’re obsessed with what it cost us to buy an investment. The cost of our investment is not just a financial commitment made by us - its also an emotional decision about ourselves. We like to think we were right. If the price of a stock moves up after we buy it, we take it as evidence of our intelligence and investing skills.

However, if it falls well below our cost, we tend to overlook negative developments about the company which we learn about subsequent to our purchase - or we tend to under-weigh such information, for example, by deluding ourselves into believing that the adversity our company is facing is only of a short term nature, and that its only a matter of time when our stock will soar.

We consciously ignore other alternative investment opportunities that become available to us, because we don’t want to buy them from cash realized from the sale of a dud investment. We fear that if we sell, we will suffer a loss, not realizing that the loss happened the day we made the wrong decision. We forget a fundamentally sound economic principle that, with a few exceptions, sunk costs i.e. what it cost us to buy a stock, are irrelevant in the sell decision.

Here’s an experiment I would recommend to all of you. Take a look at your portfolio without considering what it cost you to buy those investments. All you have is the name of each stock, the number of shares you own, the current stock price of each investment, and its current market value. Total up the last column to estimate the liquidation value of your portfolio. Notice, you’ve no idea about the cost of the individual investment, or of the entire portfolio.

Now, as objectively as you possibly can, ask yourself this question: “If I did not own all these stocks, but instead had the cash equal to their current market value, then would I buy them today?” Ask this question about every stock that is present in your portfolio. Sometimes the answer will be overwhelmingly “yes”. But when the answer is overwhelmingly “no”, you’ve to ask yourself as to why is the stock in your portfolio in the first place!

The reason why this experiment is useful is because it forces you to forget about the cost. It also forces you to start from a clean slate. When you start from a clean slate, your old past decisions will often appear to be silly, especially when they are compared with other, better alternatives. When you leave the baggage of past decisions behind, and start from a clean slate, you tend to become more rational.

The “sunk cost fallacy” is often reinforced by what is called as the “endowment effect” which shows that once you own something, you value it higher than before you owned it even though there is no rational reason for it.

Somehow, in our minds, our ownership of something wrongly increases its value. For example, just after placing bets, bettors at the racetrack become much more confident about their horse’s chance of winning the race. And lottery ticket buyers tend to buy more frequently if they are allowed to choose their own lottery tickets than when they are not. They also value their lottery tickets more highly if they personally chose them.

In a fascinating experiment, two groups of people were sold lottery tickets with identical chance of winning. Members of one group were allowed to choose their own tickets, while members of the other group were given randomly selected tickets. Immediately after the sale of tickets, but well before the results of the lottery were to be announced, members of both groups were individually asked to quote a price at which they would be willing to sell their tickets. The average quoted price for first group - those who were allowed to select their own tickets - was four times the average quoted price of the second group! Clearly, the act of buying the lottery tickets, when combined with the act of choosing the tickets themselves, magically increased their value to the first group.

There are vast practical implications of these simple experiments for you, dear reader. For you’re going to make mistakes. It’s inevitable that you will make mistakes in your buying decisions. You will face tremendous pressures that will tempt you rationalize your mistakes and not correct them. Your will tend to protect the status quo by inventing new reasons to hold on to a dud investment. This will be especially true when your original buying decision is known to many other people who are important to you. For it will hurt you to acknowledge to them, and to yourself, that you made a mistake, and it will be difficult for you to correct it because, ironically, you will attach more importance to saving face by appearing to be consistent with your past commitments, than trying to become a rational investor.

Contrary to what we may choose to believe, the functional equivalent of Mary Meeker is there in all of us.

Note:

The above piece was published in Outlook Profit, a new fortnightly magazine published by the Outlook group. Reproduced with permission.

Monday, April 21, 2008

Thursday, April 03, 2008

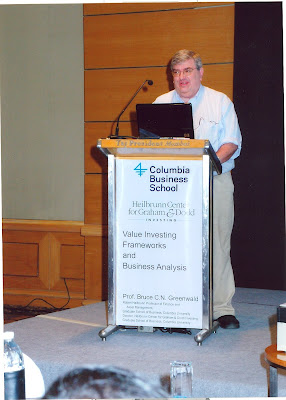

Prof. Bruce Greenwald's Talk on Value Investing

On January 8, I had the privilege of co-hosting (along with Dhananjay Lodha of Anagram and Chetan Parikh of Jeetay Investments) a talk on value investing delivered by Prof. Bruce Greenwald of Columbia Business School.

The talk, titled, "Value Investing Frameworks and Business Analytics" was delivered by Prof. Greenwald to an audience of 220 guests from the Indian investment community at Hotel Taj President in Mumbai.

Enrin Bellissimo, Director, Heilbrunn Center for Graham & Dodd Investing, and her colleague, Indira Almadi, gave us their enormous co-operation in organizing this function. Many thanks to both! Many of my ex-students helped me as well - I thank all of you.

Its interesting to know that Prof. Greenwald said that the Indian markets were over valued and due for a correction on the very day the market hit its all time high. On 8 Jan, Nifty closed at 6,287.85 points. As of the date of this writing, Nifty sands at 4,754.20. Thats a decline of 24%.

Since Prof. Greewald's talk, Nifty Midcap 50 Index has declined by 39%.

Over the same period, Nifty's P/E has fallen from 28 to 21 and Nifty Midcap 50's P/E has fallen from 24 to 14.

Prof Greenwald's presentation can be seen from here. (Uploaded with permission).

Here are a few photographs covering the function:

The talk, titled, "Value Investing Frameworks and Business Analytics" was delivered by Prof. Greenwald to an audience of 220 guests from the Indian investment community at Hotel Taj President in Mumbai.

Enrin Bellissimo, Director, Heilbrunn Center for Graham & Dodd Investing, and her colleague, Indira Almadi, gave us their enormous co-operation in organizing this function. Many thanks to both! Many of my ex-students helped me as well - I thank all of you.

Its interesting to know that Prof. Greenwald said that the Indian markets were over valued and due for a correction on the very day the market hit its all time high. On 8 Jan, Nifty closed at 6,287.85 points. As of the date of this writing, Nifty sands at 4,754.20. Thats a decline of 24%.

Since Prof. Greewald's talk, Nifty Midcap 50 Index has declined by 39%.

Over the same period, Nifty's P/E has fallen from 28 to 21 and Nifty Midcap 50's P/E has fallen from 24 to 14.

Prof Greenwald's presentation can be seen from here. (Uploaded with permission).

Here are a few photographs covering the function:

Tuesday, April 01, 2008

Fooled by a Percentage Into Catching Falling Knife!

One of my favorite experiments in class involves asking my students the following question:

“Suppose that you visit a furniture store in a mall to buy a lamp for your bedroom. You find a lamp you like and it has a list price of Rs. 5,000. Happy with this deal, when you approach the sales representative ready to buy the lamp you picked, she informs you that one of their stores which is just a ten-minute walk from there is closing down and you can buy the same lamp over there for Rs 1,000 less. Please raise your hand if the 20% discount is sufficient incentive for you to walk ten minutes to the other store to buy your lamp.”

About 70% of the students raise their hands.

My next question is then addressed to only those who raised their hands. I ask them:

“Suppose that you visit a car showroom to buy a car and after checking out many models, you find one you like. It costs Rs. 500,000, you are told by the sales representative. However, she also informs you that one of their showrooms which was just a ten-minute walk from there is closing down and you can buy the same car over there for Rs. 499,000 or Rs. 1,000 less. How many of you would like to walk ten minutes to go over to the other showroom to save Rs. 1,000?”

I hardly see a hand raised.

Somehow, students who were happy to walk ten minutes to save Rs 1,000 on a lamp are reluctant to walk ten minutes to save Rs. 1,000 on a car!

What is going on here?

Indeed, when I reframe both questions again, in a different form, students appeared puzzled:

“Would you walk ten minutes to increase your net worth by Rs. 1,000?”

Why would a man decline to save Rs 1,000 in one situation, and gladly accept it in another, with the same effort required in both situations?

Isn’t a penny saved a penny earned,?

To most people, apparently not, suggests research in behavioral economics. Part of the reason is a bias arising out of a phenomenon called the “contrast effect” which deals with how we treat multiple pieces of information presented to us one after the other.

If you put something sweet in your mouth immediately after tasting a lemon, it will taste much sweeter than it really is. The contrast between sweet and sour gets accentuated if one experiences one taste immediately after the other.

If you meet someone very attractive at a party, and immediately after that you are introduced to someone who, in contrast, is merely average looking, then the average person would appear to be more unattractive to you than would have been the case had you not met the very attractive person beforehand.

Similarly, a saving of Rs. 1,000 looks much bigger than it really is when it is contrasted with a purchase price of Rs 5,000 for a lamp, (a 20 percent saving!) but looks much smaller than it really is when it is contrasted with a purchase price of Rs 500,000 for a car (only 0.2 percent saving).

It does not matter to a man that a Rs 1,000 saving will have the same effect on his net worth whether he saves it on a lamp or a car. Somehow the presence of a 20 percent reduction triggers an irrational response in his brain.

The brain, operating at the subconscious level, is often influenced by the presence of false “anchors”. Anchors are pieces of information to which a mind tends to latch on to while making a decision. And the human mind will often latch on to false anchors created by various influences like availability or contrast.

In a classic experiment, researchers asked a group of people if the Mississippi River in the US is longer or shorter than 500 miles (the anchor). Most people responded that it was longer than 500 miles. They were then asked to estimate the length of that river. The average answer was about 1,000 miles.

A second group, in contrast, was asked if the Mississippi River is longer or shorter than 5,000 miles and were then asked to estimate its length. Most people responded that it was shorter than 5,000 miles but the average length of the River in this group was about 2,000 miles!

The actual length of the Mississippi River is 2,348 miles but false anchors of 500 miles or 5,000 miles tend to pull the average answers towards them!

In the lamp vs. car experiment, students who chose to walk ten minutes to save Rs 1,000 while buying a lamp but who refused to walk ten minutes to save the same amount of money while buying a car, were suffering from “anchoring bias”. Their minds were latching on to the wrong anchor of a large percentage savings on a list price, instead of latching on to the right anchor of their personal net worth.

Anchors are important, of course, but one has to be careful when deciding if an anchor is valid or not. A man who feels miserable because he dropped Rs. 500 from his pocket which had only Rs. 1,000 in it even though his personal net worth is Rs. fifty lacs is suffering from an anchoring bias. He incorrectly identifies the money in his pocket as a valid anchor as opposed to his net worth. He is also suffering from bias arising out of contrast effect because Rs 500 lost out of Rs 1,000 in his pocket looks very big to him in percentage terms.

In contrast, a rational investor who practices wide diversification, knows that its inevitable that some of his picks will turn out to be duds. He does, not, however, let such outcomes make him miserable because he has trained himself to latch on to the right anchors such as the size of his portfolio, and not the percentage lost in a single position.

A stock may have fallen 50 percent from its all-time peak in a market crash, may have gone below its 52-week low price, may have fallen below the price at which its shares were offered in a hot IPO, or may have fallen below par value. None of these things mean that the stock is cheap. A stock is cheap only if its price has fallen well below than what the company is rationally worth on a per-share basis.

In contrast with underlying value which is the right anchor to latch on to, all time peak prices, 52-week low price, IPO price, and par value are all false anchors. If you blindly buy stocks merely because they have fallen well below some false anchors, thereby allowing contrast effect to make you feel that they are much cheaper than they really might be, then you are functionally equivalent to the man who is trying to catch a falling knife.

And that, you will agree, can hurt.

Sanjay Bakshi is a Visiting Professor at Management Development Institute, Gurgaon. www.sanjaybakshi.net

Note:

The above piece was published in Outlook Profit, a new fortnightly magazine published by the Outlook group. Reproduced with permission.

“Suppose that you visit a furniture store in a mall to buy a lamp for your bedroom. You find a lamp you like and it has a list price of Rs. 5,000. Happy with this deal, when you approach the sales representative ready to buy the lamp you picked, she informs you that one of their stores which is just a ten-minute walk from there is closing down and you can buy the same lamp over there for Rs 1,000 less. Please raise your hand if the 20% discount is sufficient incentive for you to walk ten minutes to the other store to buy your lamp.”

About 70% of the students raise their hands.

My next question is then addressed to only those who raised their hands. I ask them:

“Suppose that you visit a car showroom to buy a car and after checking out many models, you find one you like. It costs Rs. 500,000, you are told by the sales representative. However, she also informs you that one of their showrooms which was just a ten-minute walk from there is closing down and you can buy the same car over there for Rs. 499,000 or Rs. 1,000 less. How many of you would like to walk ten minutes to go over to the other showroom to save Rs. 1,000?”

I hardly see a hand raised.

Somehow, students who were happy to walk ten minutes to save Rs 1,000 on a lamp are reluctant to walk ten minutes to save Rs. 1,000 on a car!

What is going on here?

Indeed, when I reframe both questions again, in a different form, students appeared puzzled:

“Would you walk ten minutes to increase your net worth by Rs. 1,000?”

Why would a man decline to save Rs 1,000 in one situation, and gladly accept it in another, with the same effort required in both situations?

Isn’t a penny saved a penny earned,?

To most people, apparently not, suggests research in behavioral economics. Part of the reason is a bias arising out of a phenomenon called the “contrast effect” which deals with how we treat multiple pieces of information presented to us one after the other.

If you put something sweet in your mouth immediately after tasting a lemon, it will taste much sweeter than it really is. The contrast between sweet and sour gets accentuated if one experiences one taste immediately after the other.

If you meet someone very attractive at a party, and immediately after that you are introduced to someone who, in contrast, is merely average looking, then the average person would appear to be more unattractive to you than would have been the case had you not met the very attractive person beforehand.

Similarly, a saving of Rs. 1,000 looks much bigger than it really is when it is contrasted with a purchase price of Rs 5,000 for a lamp, (a 20 percent saving!) but looks much smaller than it really is when it is contrasted with a purchase price of Rs 500,000 for a car (only 0.2 percent saving).

It does not matter to a man that a Rs 1,000 saving will have the same effect on his net worth whether he saves it on a lamp or a car. Somehow the presence of a 20 percent reduction triggers an irrational response in his brain.

The brain, operating at the subconscious level, is often influenced by the presence of false “anchors”. Anchors are pieces of information to which a mind tends to latch on to while making a decision. And the human mind will often latch on to false anchors created by various influences like availability or contrast.

In a classic experiment, researchers asked a group of people if the Mississippi River in the US is longer or shorter than 500 miles (the anchor). Most people responded that it was longer than 500 miles. They were then asked to estimate the length of that river. The average answer was about 1,000 miles.

A second group, in contrast, was asked if the Mississippi River is longer or shorter than 5,000 miles and were then asked to estimate its length. Most people responded that it was shorter than 5,000 miles but the average length of the River in this group was about 2,000 miles!

The actual length of the Mississippi River is 2,348 miles but false anchors of 500 miles or 5,000 miles tend to pull the average answers towards them!

In the lamp vs. car experiment, students who chose to walk ten minutes to save Rs 1,000 while buying a lamp but who refused to walk ten minutes to save the same amount of money while buying a car, were suffering from “anchoring bias”. Their minds were latching on to the wrong anchor of a large percentage savings on a list price, instead of latching on to the right anchor of their personal net worth.

Anchors are important, of course, but one has to be careful when deciding if an anchor is valid or not. A man who feels miserable because he dropped Rs. 500 from his pocket which had only Rs. 1,000 in it even though his personal net worth is Rs. fifty lacs is suffering from an anchoring bias. He incorrectly identifies the money in his pocket as a valid anchor as opposed to his net worth. He is also suffering from bias arising out of contrast effect because Rs 500 lost out of Rs 1,000 in his pocket looks very big to him in percentage terms.

In contrast, a rational investor who practices wide diversification, knows that its inevitable that some of his picks will turn out to be duds. He does, not, however, let such outcomes make him miserable because he has trained himself to latch on to the right anchors such as the size of his portfolio, and not the percentage lost in a single position.

A stock may have fallen 50 percent from its all-time peak in a market crash, may have gone below its 52-week low price, may have fallen below the price at which its shares were offered in a hot IPO, or may have fallen below par value. None of these things mean that the stock is cheap. A stock is cheap only if its price has fallen well below than what the company is rationally worth on a per-share basis.

In contrast with underlying value which is the right anchor to latch on to, all time peak prices, 52-week low price, IPO price, and par value are all false anchors. If you blindly buy stocks merely because they have fallen well below some false anchors, thereby allowing contrast effect to make you feel that they are much cheaper than they really might be, then you are functionally equivalent to the man who is trying to catch a falling knife.

And that, you will agree, can hurt.

Sanjay Bakshi is a Visiting Professor at Management Development Institute, Gurgaon. www.sanjaybakshi.net

Note:

The above piece was published in Outlook Profit, a new fortnightly magazine published by the Outlook group. Reproduced with permission.

Subscribe to:

Posts (Atom)